Singapore’s rental market saw a noticeable slowdown in February 2026, with leasing volumes falling across both condominium and HDB segments. The pullback followed a relatively active January and was seen largely as a seasonal pause during the festive period.

Despite the decline in transactions, rental prices across the market remained relatively stable. Condo rental prices dipped slightly month-on-month, while HDB rental prices continued to inch upward. On a year-on-year basis, both segments still recorded modest price growth, suggesting that the underlying rental market remains resilient.

Table of contents

- Condo rental prices ease slightly as leasing activity tapers

- 25.5% month-on-month decrease in condo rental volumes

- HDB rental prices continue a modest upward trend

- HDB leasing activity eases 20.1% month-on-month

- Market outlook

Condo rental prices ease slightly as leasing activity tapers

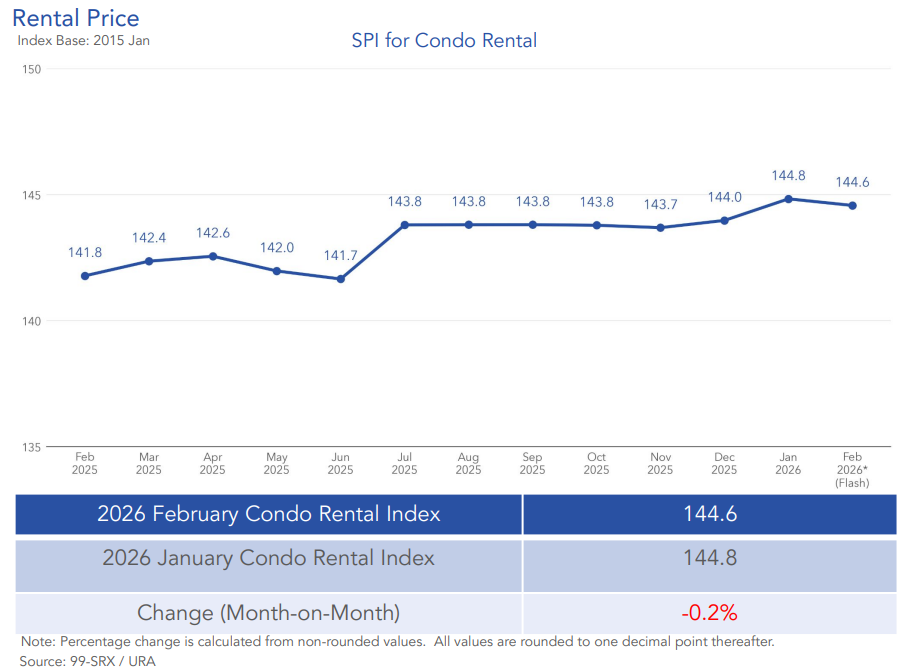

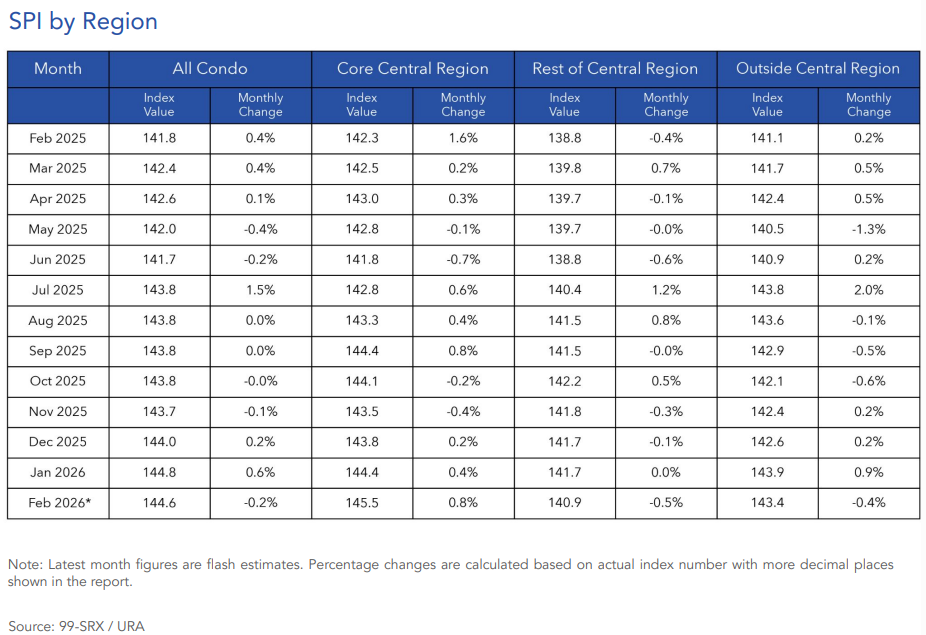

Condominium rental prices edged down slightly in February 2026, with the 99-SRX Condo Rental Price Index declining 0.2% month-on-month, easing from 144.8 in January to 144.6 in February. With softer leasing activity typically observed during the festive season, rental negotiations may lean slightly more in favour of tenants, leading to marginal adjustments in price levels.

Across Singapore’s three main regions, rental price trends were mixed. The Rest of Central Region (RCR) saw rental prices decline 0.5%, while the Outside Central Region (OCR) recorded a 0.4% drop compared to January. In contrast, the Core Central Region (CCR) — which includes many prime and centrally located developments — posted a 0.8% increase in rental prices.

This divergence may suggest that demand for centrally located homes, often favoured by expatriates and corporate tenants, remained relatively stable despite the broader slowdown in leasing activity.

Looking at the longer-term trend, the rental market still shows signs of resilience. Condo rental prices were 2% higher than a year ago, with all three regions recording annual increases. The CCR led the growth with a 2.3% year-on-year rise, while prices in the OCR and RCR increased by 1.6% and 1.5%, respectively.

25.5% month-on-month decrease in condo rental volumes

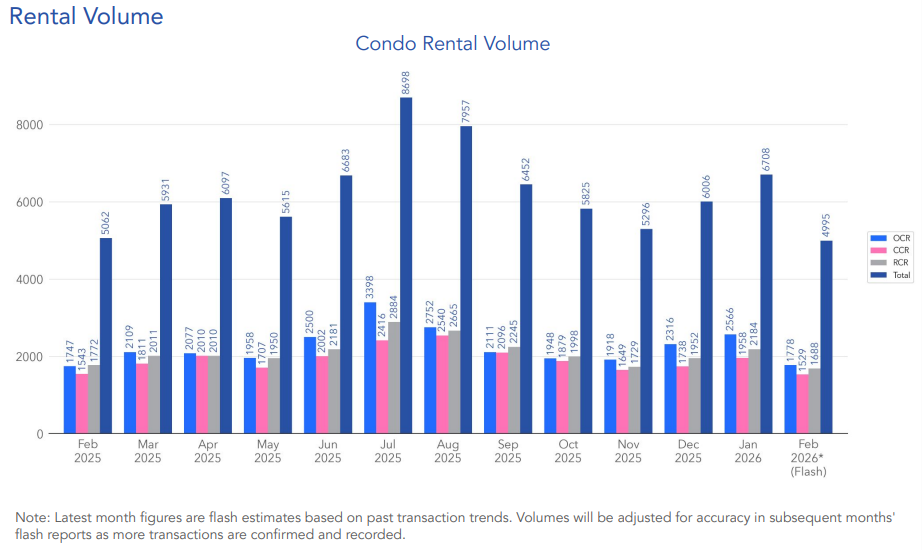

While rental prices remained relatively stable, leasing activity in the private residential market slowed more noticeably during the month. An estimated 4,995 condominium units were rented in February 2026, a 25.5% decline from the 6,708 units in January.

Compared with the same month last year, condo rental transactions were 1.3% lower than in February 2025, suggesting that overall leasing demand remains broadly similar to last year but may fluctuate month-to-month due to seasonal factors.

In addition, February’s leasing volume came in 4.5% below the five-year average for the month, reinforcing the view that activity slowed more than usual this year, possibly due to the timing of festive celebrations.

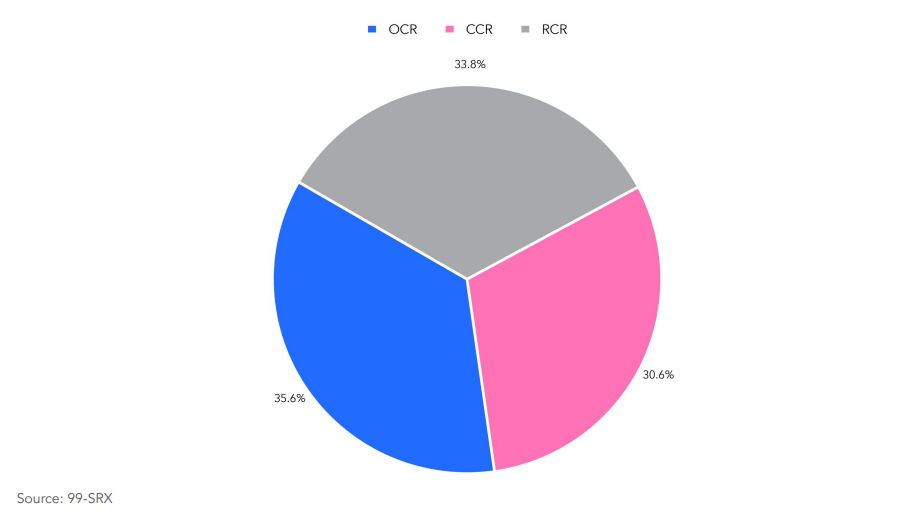

Regionally, leasing activity remained relatively balanced across the island. The OCR accounted for the largest share of rental transactions at 35.6%, reflecting continued demand for more affordable suburban rental options. Meanwhile, RCR made up 33.8% of transactions, while the CCR accounted for 30.6% of all condo rentals during the month.

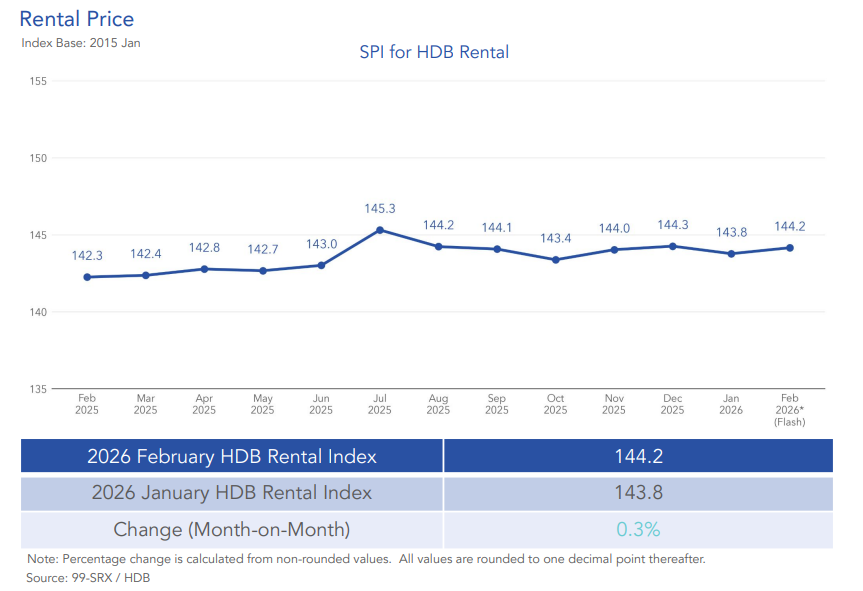

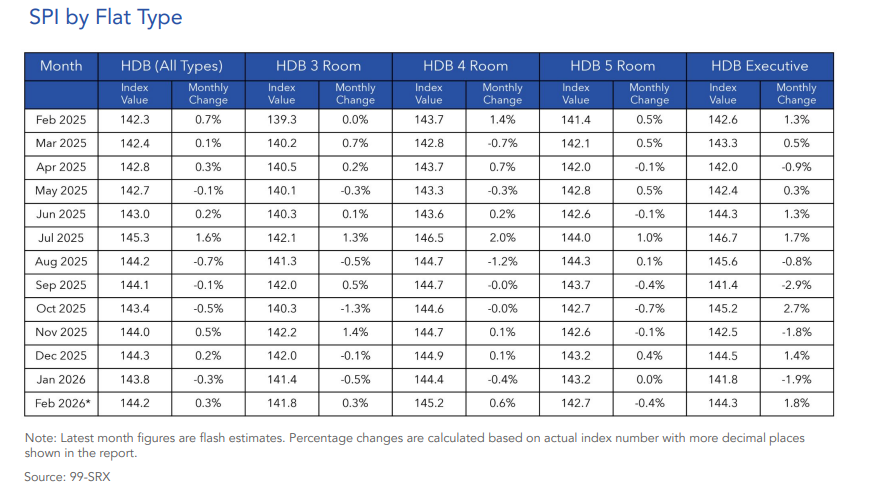

HDB rental prices continue a modest upward trend

The HDB Rental Price Index rose 0.3% month-on-month, increasing from 143.8 in January to 144.2 in February 2026.

This steady upward movement suggests that demand for public housing rentals remains relatively stable. HDB flats continue to serve as an important alternative for tenants who are priced out of the private rental market or prefer more affordable housing options.

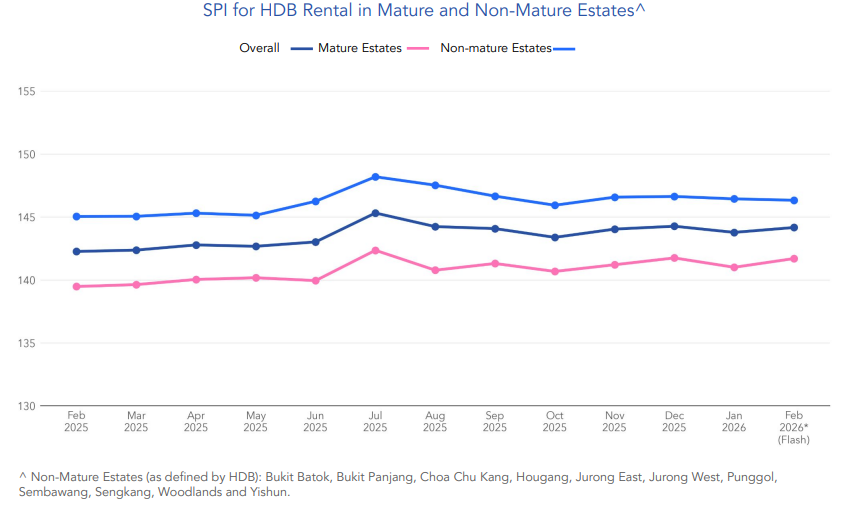

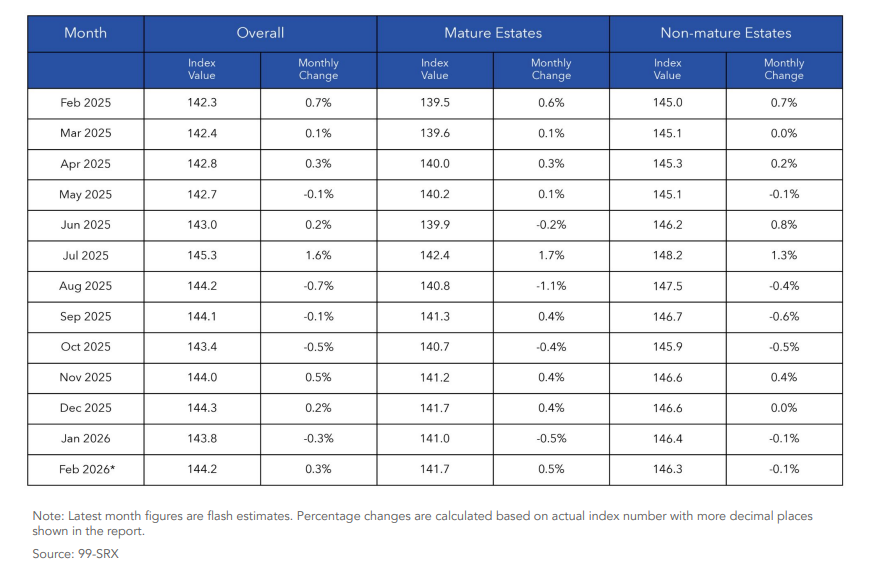

Price movements differed slightly between estate types. Mature estates recorded a 0.5% increase in rental prices, while Non-Mature estates saw a slight decline of 0.1% during the same period.

The stronger price growth in mature towns may reflect their established amenities, convenient transport connectivity, and proximity to employment centres. Locations such as Bukit Merah and the Central Area often remain popular with tenants due to their accessibility and well-developed neighbourhood infrastructure.

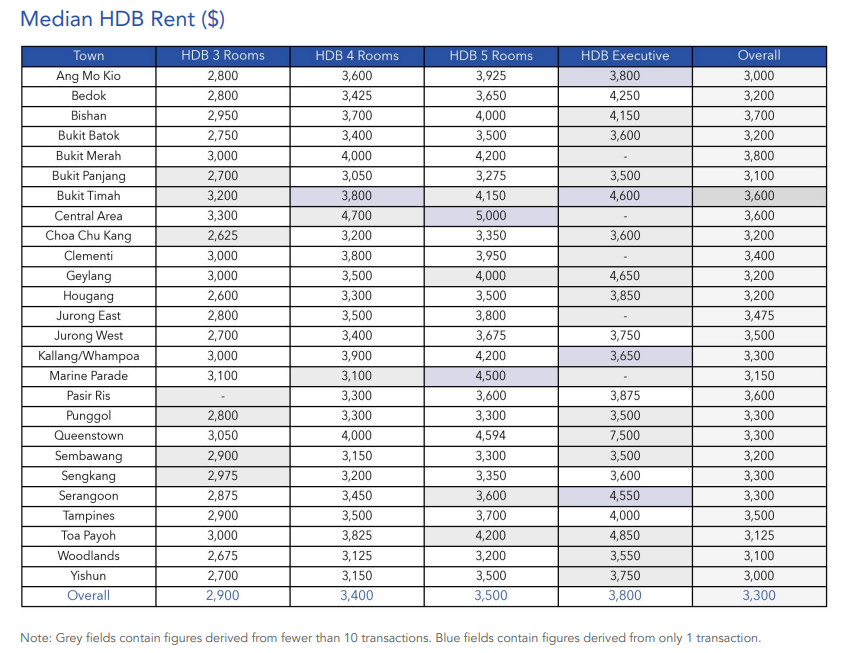

Looking at flat types, most segments recorded rental increases in February. Executive flats saw the largest monthly increase of 1.8%, followed by 4-room flats at 0.6% and 3-room flats at 0.3%. Meanwhile, 5-room flats experienced a slight decline of 0.4% during the month.

On an annual basis, HDB rental prices also continued to trend upward. Overall rental prices were 1.3% higher than in February 2025, reflecting continued demand in the public housing rental market.

By estate type, Mature estates recorded a 1.6% increase year-on-year, while Non-Mature estates saw rents rise 0.9%. Across flat types, 3-room flats led annual growth with a 1.8% increase, followed by Executive flats at 1.2%, 4-room flats at 1%, and 5-room flats at 0.9%.

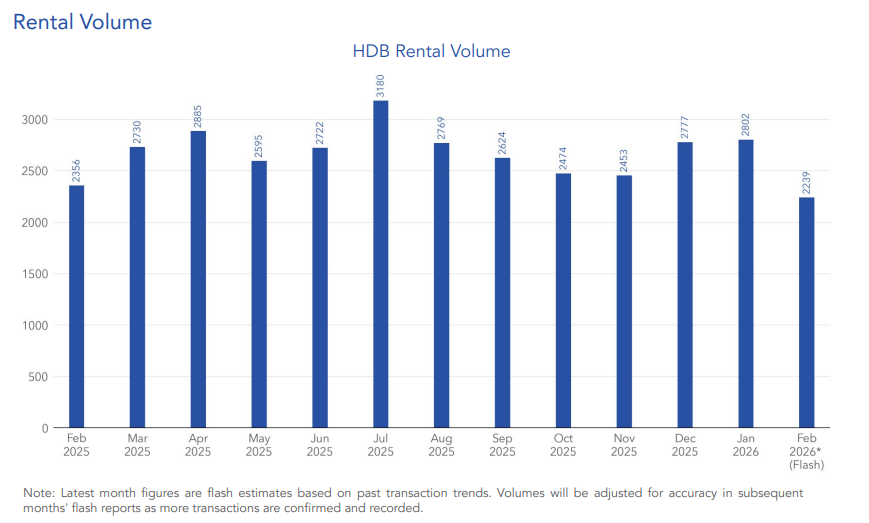

HDB leasing activity eases 20.1% month-on-month

Leasing activity for HDB flats mirrored the trend seen in the private rental market. An estimated 2,239 HDB flats were rented in February 2026, marking a 20.1% decline from the 2,802 units rented in January. On a year-on-year basis, HDB rental volumes were 5% lower than in February 2025.

Transaction volumes were also 9.7% lower than the five-year average for February, suggesting that this year’s festive slowdown may have had a slightly larger impact on the rental market.

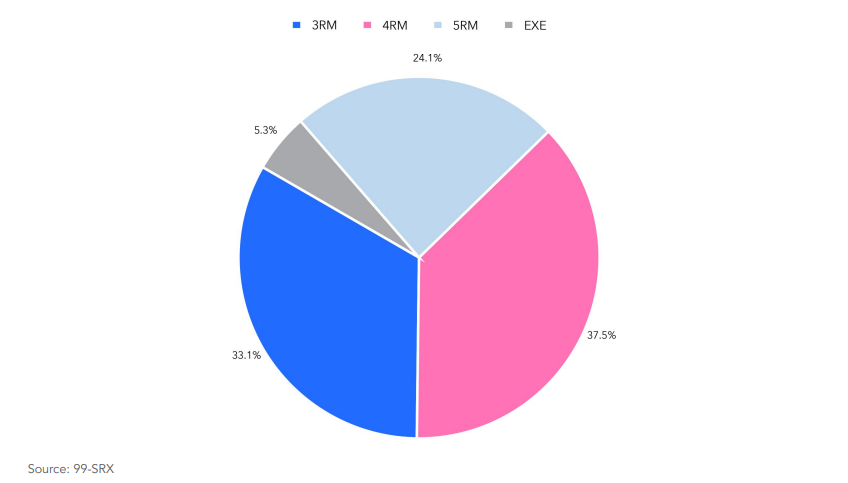

Breaking down the rental transactions by flat type, 4-room flats remained the most commonly rented unit type, accounting for 37.5% of total HDB rental transactions. This was followed by 3-room flats at 33.1%, 5-room flats at 24.1%, and Executive flats at 5.3%. The dominance of 3-room and 4-room flats highlights their continued appeal among tenants seeking a balance between affordability and space.

Market outlook

Commenting on the recent figures, Mr Luqman Hakim, Chief Data & Analytics Officer at 99.co, reinforced that the slowdown in leasing activity during February is largely seasonal.

He explained that during the Chinese New Year period, “market activity tends to moderate as households defer moving decisions, and leasing transactions are temporarily paused.” Property searches and viewings often decrease as tenants travel or prioritise family gatherings, while landlords may also postpone listing or finalising rental agreements.

Mr Luqman added that February typically records lower transaction volumes than January, a month that usually benefits from year-end relocations and tenants securing housing before the festive season begins.

Despite the seasonal dip, he noted that “the slight year-on-year price growth for both HDB and condo suggests that underlying rental demand remains resilient.” Looking ahead, leasing activity is expected to gradually recover in the months following the festive period as tenants resume relocation plans and the rental market returns to its usual pace.

The post Condo and HDB rental activity slows down in February 2026 amid festive period appeared first on .