Singapore’s rental market softened slightly for the second straight month in September 2025. Both condo and HDB rents saw small dips, but prices held relatively firm despite the slower activity. What’s behind this slowdown and what does it mean for renters and landlords heading into the rest of the year and early 2026?

Table of contents

- Condo rental prices held steady, while volumes saw a seasonal slowdown

- HDB rental prices eased slightly as volumes dipped but stayed above year-ago levels

- What can renters and landlords expect in the coming months?

Quick summary

- 📉Rental activity dipped again in Sept 2025.

- 💰Prices stayed firm despite slower demand.

Market highlights

- 🏙️~6,400 condos and ~2,600 HDB flats rented.

- 📆September holidays slowed leasing activity.

- 🔮Rents expected to hold steady into early 2026.

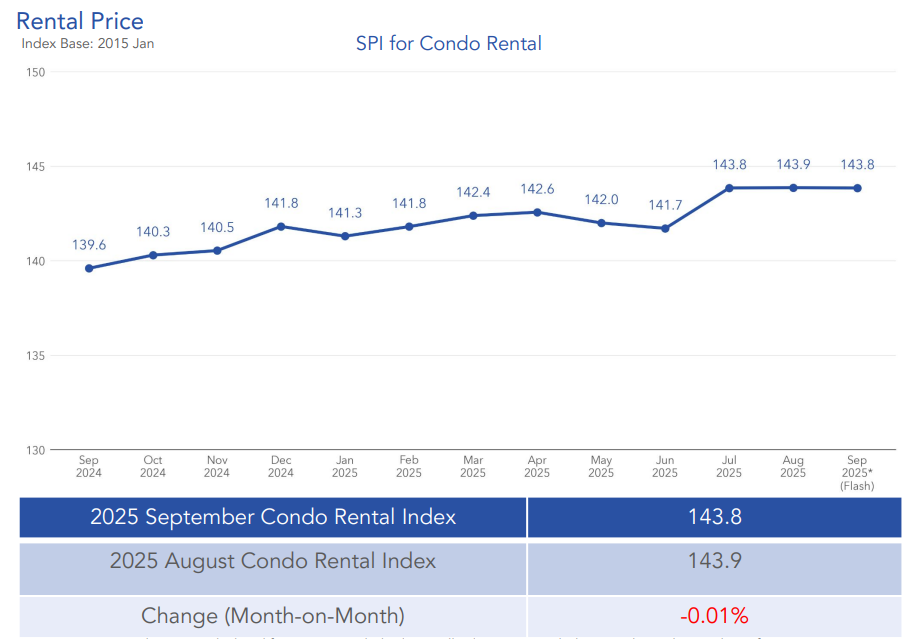

Condo rental prices held steady, while volumes saw a seasonal slowdown

In September 2025, overall condo rents were largely stable, slipping by just 0.01% month-on-month. Across regions, performance varied slightly – rents in the Core Central Region (CCR) rose 0.8%, while those in the Outside Central Region (OCR) fell 0.5%. Meanwhile, the Rest of Central Region (RCR) stayed unchanged from August.

Year-on-year, condo rents were up by 3%, showing that despite recent easing, prices remain resilient. Over the same period, CCR rents climbed 3.6%, RCR rents increased 3%, and OCR rents rose 2.7%. These figures point to steady demand in all regions, even as price growth moderates from the rapid gains seen in previous years.

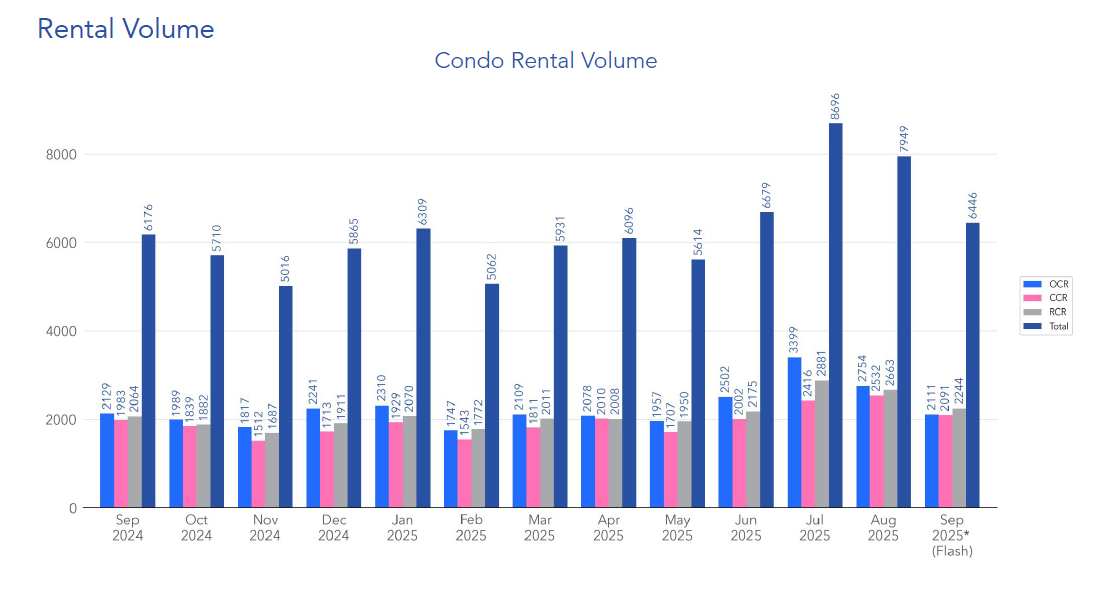

When it comes to leasing activity, though, there was a more noticeable drop. Rental volumes fell by 18.9% month-on-month, with an estimated 6,446 units rented in September – down from 7,949 units in August. This marks one of the sharpest declines in monthly activity this year. However, on an annual basis, volumes were still 4.4% higher than in September 2024 and only 0.8% below the five-year average for the same month.

Breaking it down further, about 32.7% of total rental transactions came from OCR, 34.8% from RCR, and 32.4% from CCR. This balanced distribution shows that tenants continue to be active across all regions, though the overall pace has slowed.

Mr. Luqman Hakim, Chief Data & Analytics Officer at 99.co, noted that “the slower leasing activity in September is not unusual, as many potential tenants, particularly expatriates, tend to wait until the final quarter before securing new leases.” He added that “limited new completions and firm landlord expectations have helped rents remain stable, even as some demand temporarily eases.”

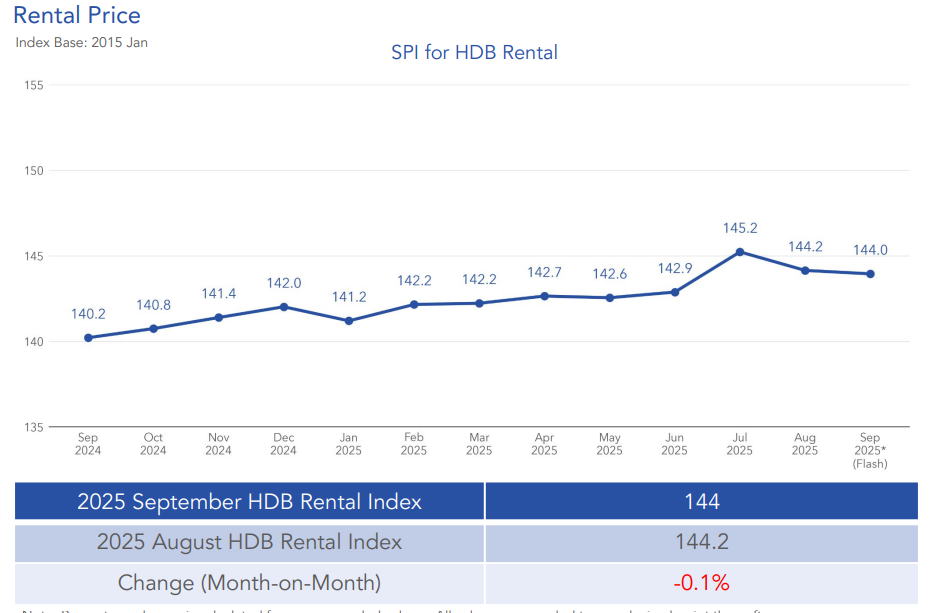

HDB rental prices eased slightly as volumes dipped but stayed above year-ago levels

The HDB rental segment followed a similar trend, showing a slight cooling after months of steady growth. Overall, HDB rents dipped 0.1% month-on-month in September 2025. Prices in Mature towns inched up 0.3%, while those in Non-Mature towns declined 0.6%.

Among the various flat types, only 3-room units saw prices rise by 0.6%. In contrast, 4-room, 5-room, and Executive flats fell by 0.1%, 0.4%, and 3%, respectively.

Even with these small monthly dips, overall HDB rents were still 2.7% higher year-on-year. Mature estates recorded a 3.3% annual increase, while Non-Mature estates rose 1.8%. Across flat types, 3-room, 4-room, and 5-room units grew 3.7%, 2.2%, and 2.3%, respectively, compared with a slight 0.1% drop for Executive flats.

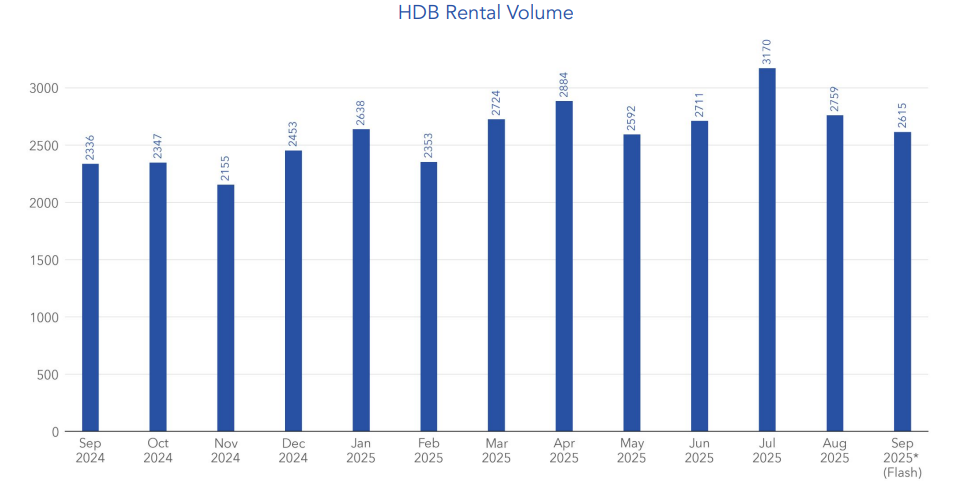

Leasing volumes also moderated. About 2,615 HDB flats were rented in September, down 5.2% from 2,759 units in August. Even so, activity was 11.9% higher than last year and 7.3% above the five-year average, suggesting that overall demand remains firm despite the seasonal dip. By room type, 33.7% of rentals were 3-room, 36.6% were 4-room, 24.5% were 5-room, and 5.1% were Executive flats.

Commenting on the HDB market, Mr. Luqman Hakim shared that “the September school break tends to affect HDB rentals as well, especially since many family tenants prefer to move after the holidays.” He added that “tight vacancy rates and a steady stream of demand have kept prices from dropping significantly.”

This pattern suggests that while activity may fluctuate month to month, the fundamentals behind HDB rental demand remain strong – a sign of stability even in a slower season.

What can renters and landlords expect in the coming months?

Although September was quieter, the overall rental landscape remains firm. “We’re seeing what could be described as a soft landing after several years of strong rental growth,” said Mr. Luqman. “Rents are expected to hold steady into late 2025, with leasing activity likely to pick up toward the year’s end.”

You can expect the addition of new private and public housing units to bring some relief to tenants, especially those looking for more affordable options. However, underlying demand – supported by stable employment levels, population growth, and ongoing relocations – should keep prices broadly stable well into early 2026.

For renters, this means that while prices may not fall sharply, competition for well-located units could ease slightly. For landlords, maintaining realistic rent expectations will help ensure smoother leasing in the months ahead.

As the market gradually finds its balance, Singapore’s rental sector appears to be transitioning into a more sustainable phase – one where demand remains healthy but price growth is steady rather than steep.

The post Rental activity softened again, yet prices remained firm in September 2025 appeared first on .