January 2026 opens the year with a familiar pattern in Singapore’s condo resale market. Resale prices edged up slightly, even as transaction volumes continued to slip since the fourth quarter of last year.

Commenting on the latest flash estimates, Mr Luqman Hakim, Chief Data & Analytics Officer at 99.co, explained that “the moderation in volumes, coupled with stable to modestly rising prices, points to a market that remains steady while adjusting to a more measured buying sentiment”.

Table of contents

- Overall condo resale prices rose 0.5% month-on-month

- 3.5% drop in volumes compared to December 2025

- Sub-sales decline — Less speculative resale activity

- Median capital gains in January 2026: S$380,000

- Median unlevered returns for condo resale: 29.4%

- High-value resale deals across the regions

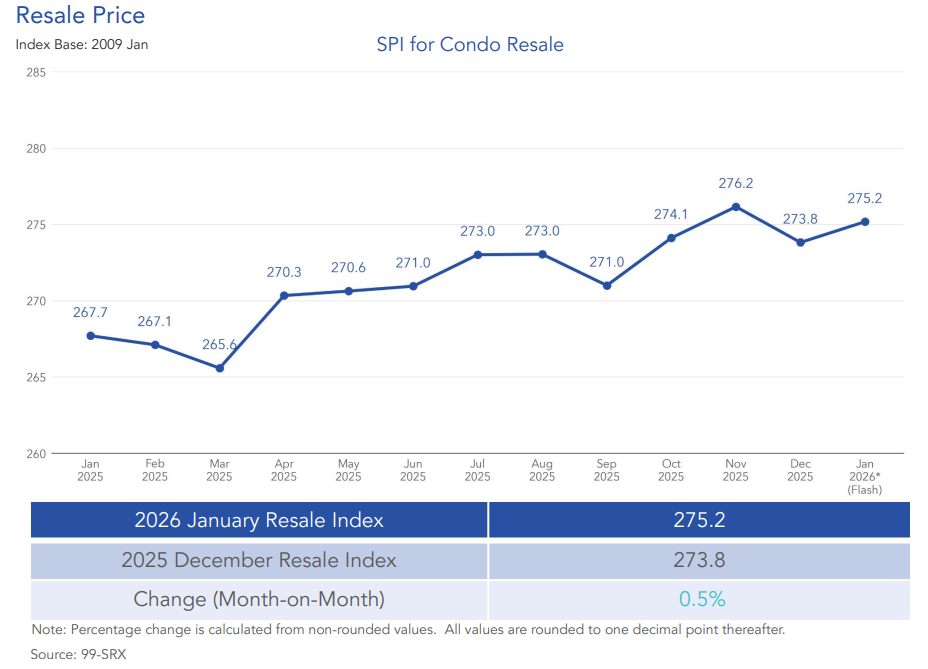

Overall condo resale prices rose 0.5% month-on-month

According to the 99-SRX Price Index for condo resale, overall prices rose by 0.5% in January 2026. The resale index climbed from 273.8 in December 2025 to 275.2 in January.

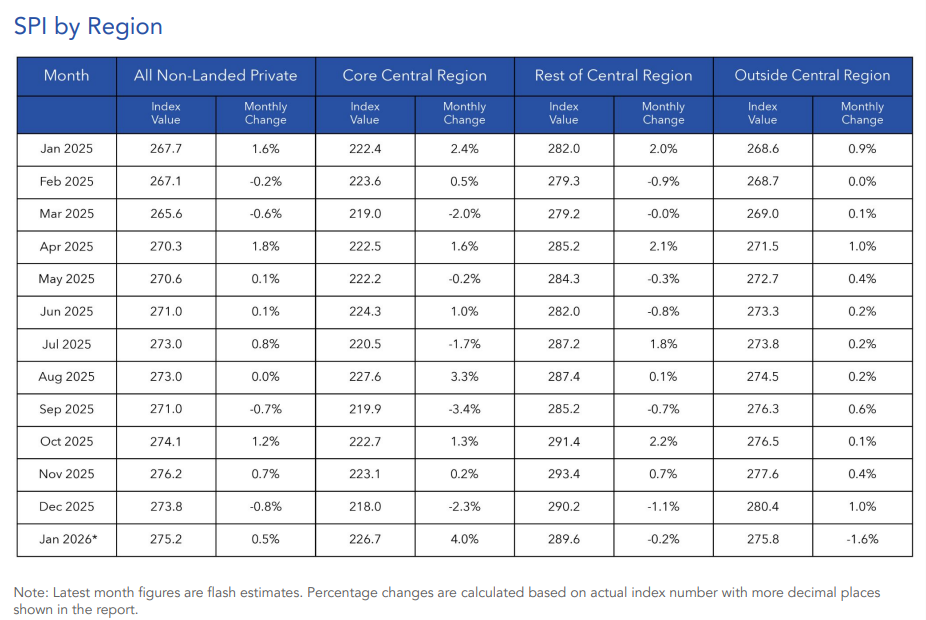

On a year-on-year basis, prices increased by 2.8% compared to January 2025. All three regions remain in positive territory, indicating that underlying price support remains intact despite a more cautious demand environment.

- Core Central Region (CCR): up 1.9% year-on-year

- Rest of Central Region (RCR): up 2.7% year-on-year

- Outside Central Region (OCR): up 2.7% year-on-year

The month-on-month performance, however, showed divergence across regions. CCR prices rose by 4% in January 2026, while RCR and OCR prices dipped by 0.2% and 1.6%, respectively. The slight pullback in RCR and OCR suggests some resistance at higher price points in the mass and city-fringe segments.

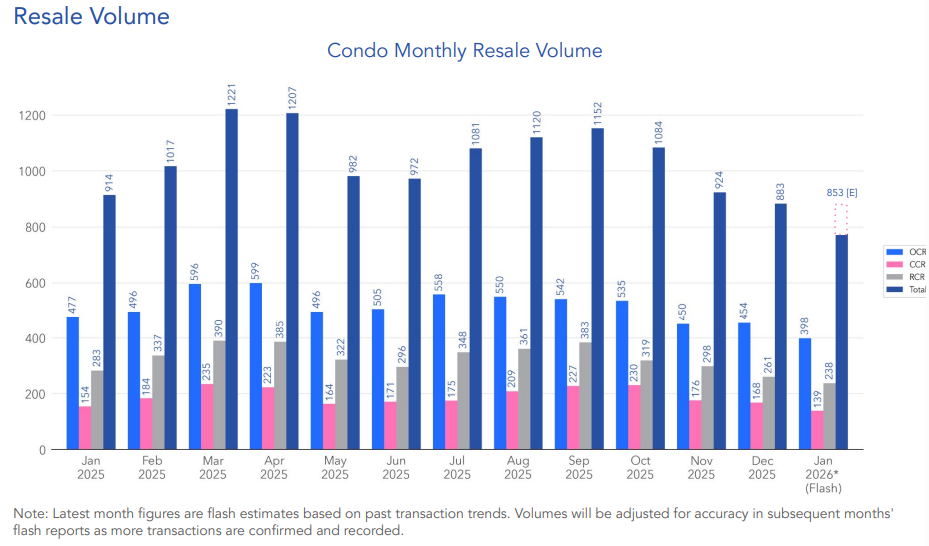

3.5% drop in volumes compared to December 2025

An estimated 853 condo units were resold in January 2026. That represents a 3.5% decline from December’s 883 units and a 6.7% drop compared to January 2025. Activity also came in 0.4% below the five-year January average, suggesting a slightly softer-than-usual start to the year.

For homeowners watching the numbers, falling volume can trigger resale concern. However, considering past trends, resale activity is expected to pick up in the coming months.

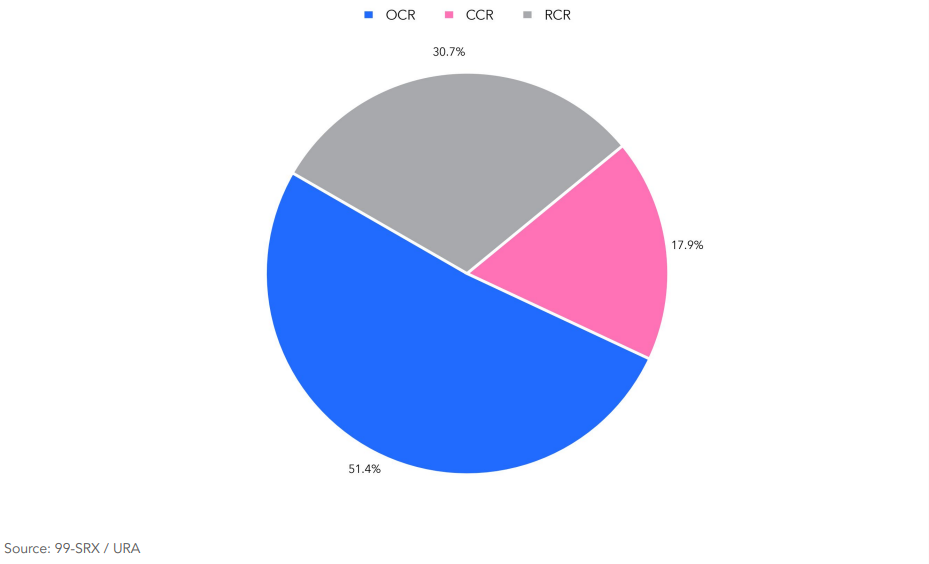

In January 2026, OCR still accounted for more than half of all resale transactions at 51.4%, with RCR making up 30.7% and CCR contributing 17.9%. This distribution highlights that the mass market remains the backbone of resale activity.

The moderation in overall activity, coupled with OCR accounting for the majority of transactions, points to several underlying structural dynamics. First, affordability pressures remain visible. Easing volumes reveals a more cautious, value-driven buyer pool. At the same time, price stickiness among sellers limits deal flow. Without financial pressure to sell, they resist cutting prices significantly.

This creates a natural stand-off in the market, where transactions only occur when both sides find a pricing sweet spot. As Mr Luqman explained, “While sellers are generally maintaining pricing expectations, buyers are proceeding more selectively, focusing on securing the right value and quality.”

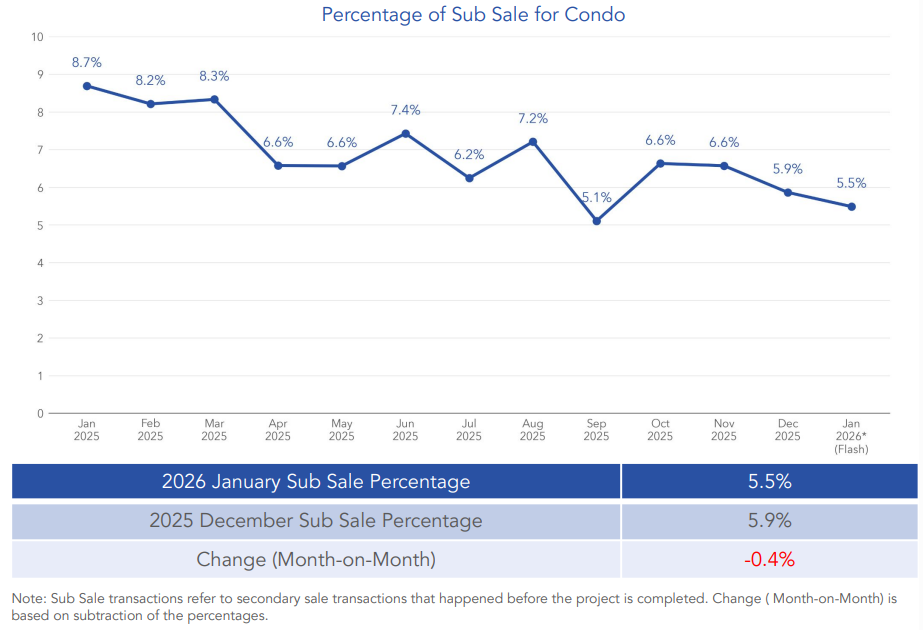

Sub-sales decline — Less speculative resale activity

Sub-sale transactions made up 5.5% of total secondary sales in January, down from 5.9% in December. Sub-sales occur when units are sold before project completion.

A declining sub-sale percentage suggests reduced short-term flipping activity. This matters because high sub-sale activity often correlates with speculative cycles. The current low proportion indicates that most resale transactions involve completed projects and longer-term ownership.

For sellers and buyers, this is a stabilising factor. A resale market driven by genuine owner-occupiers and long-term investors tends to be less volatile.

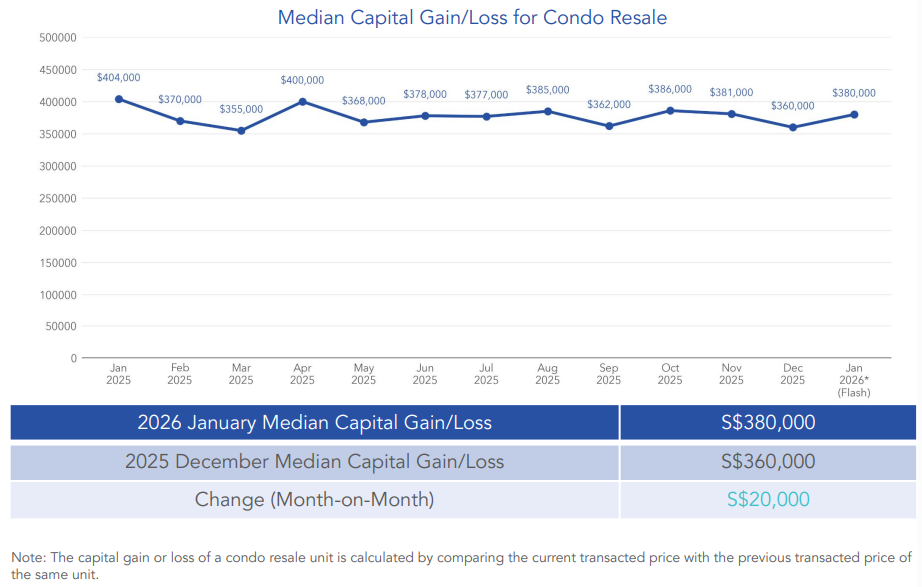

Median capital gains in January 2026: S$380,000

The overall median capital gain for January stood at S$380,000, up from S$360,000 in December. This S$20,000 increase shows that profitability remains intact for many sellers.

Capital gains are calculated by comparing each unit’s current transaction price with its previous sale price. While individual experiences vary, the median figure provides a broad snapshot of performance.

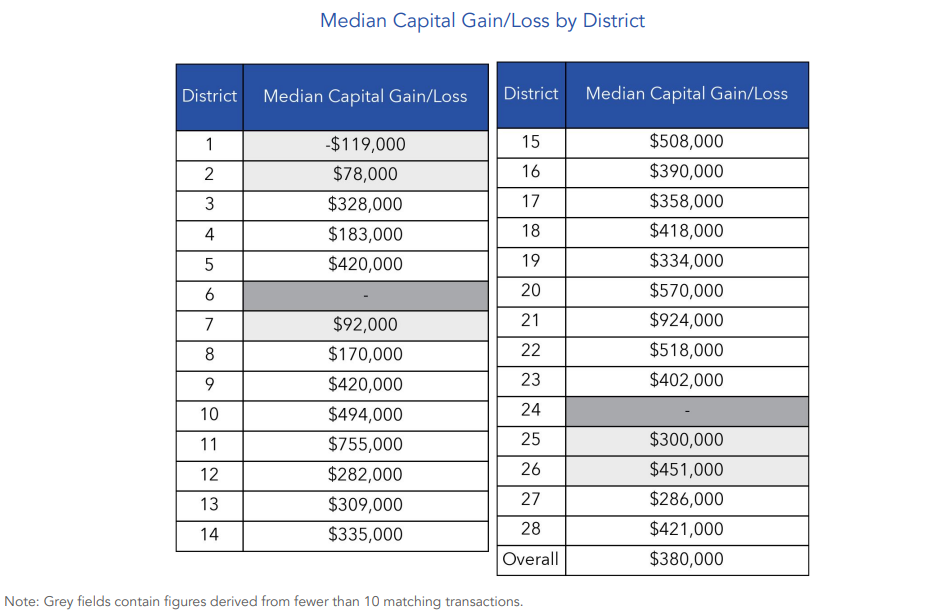

District-level data shows a wide range of outcomes:

- District 21 (Clementi Park / Upper Bukit Timah) recorded the highest median capital gain at S$924,000.

- District 8 (Farrer Park / Serangoon Road) posted the lowest median capital gain at S$170,000.

The strength in District 21 likely reflects longer holding periods, family-oriented demand, and sustained appeal near established schools and lifestyle amenities. Areas with strong underlying fundamentals continue to outperform.

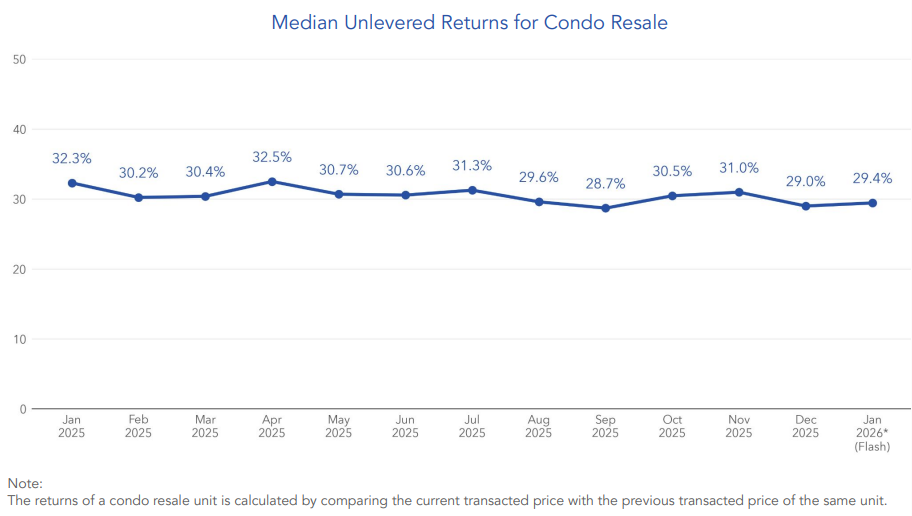

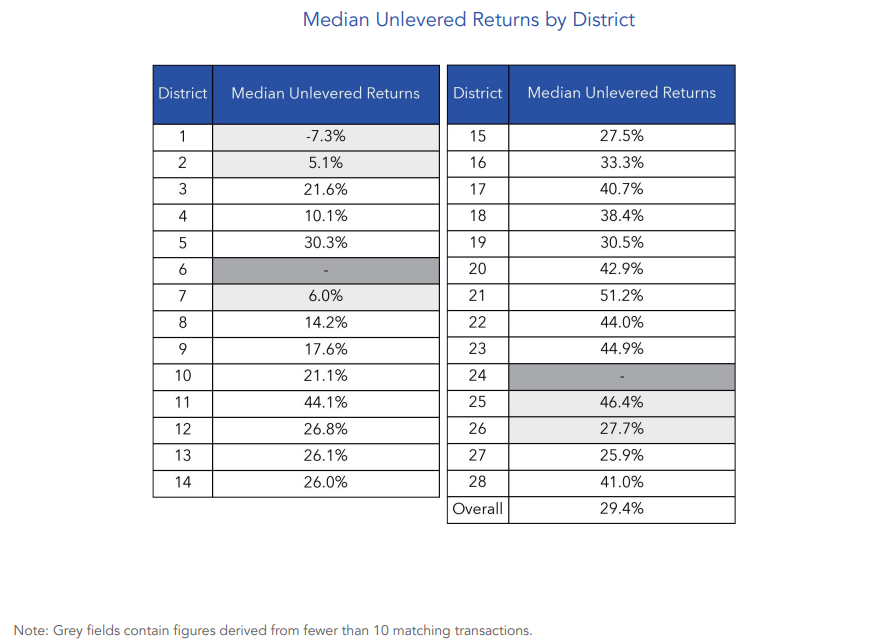

Median unlevered returns for condo resale: 29.4%

Beyond absolute gains, the median unlevered return for resale condos stood at 29.4% in January 2026. Unlevered returns measure percentage gains without factoring in financing. This metric provides a clearer view of asset appreciation performance over time.

District 21 again topped the table with a median unlevered return of 51.2%. In contrast, District 4 (Sentosa / Harbourfront) recorded the lowest median unlevered return at 10.1%.

While returns remain healthy overall, the spread between districts underscores a key point: not all locations perform equally. Asset selection remains critical in today’s environment.

Investors who entered projects with strong fundamentals — connectivity, school proximity, and consistent demand — continue to see stronger returns. Projects with niche appeal or limited buyer pools experience more modest appreciation.

High-value resale deals across the regions

Despite overall softer activity, several high-value resale transactions still stood out in January 2026. While such deals can be eye-catching, they remain the exception rather than the norm.

CCR: S$37,000,000 at The Marq on Paterson Hill

The highest resale transaction recorded in January was an eye-catching S$37 million deal at The Marq on Paterson Hill in District 9. Located along Paterson Hill, just off Orchard Road, the development sits firmly within Singapore’s prime luxury belt and caters to a niche ultra-high-net-worth buyer segment.

Developed by SC Global Developments, this freehold project was completed in 2011 and comprises only 66 units, reinforcing its low-density, high-privacy positioning. The Marq on Paterson Hill features two 24-storey towers. The Premier Tower offers 4-bedroom units of 3,089 sqft, while the Signature Tower features 4-bedroom units of 6,232 sqft, each with a double-volume ceiling and a private lap pool.

RCR: S$6,200,000 at Maple Woods

In the Rest of Central Region, the highest resale price recorded in January was S$6.2 million at Maple Woods. Situated along Bukit Timah Road in District 21, Maple Woods is a freehold leasehold development completed in 1997 by Wing Tai Holdings. The project comprises 697 units across multiple residential blocks set within a lush, resort-style landscape.

Known for its generous site and extensive greenery, Maple Woods appeals strongly to families seeking space within a central location. The development comprises 2- to 4-bedders measuring between 850 and 3,003 sqft. It is located within walking distance of King Albert Park MRT Station on the Downtown Line, which is set to become an interchange station once Phase 2 of the Cross Island Line commences operations in 2032.

OCR: S$4,500,000 at Bedok Residences

Meanwhile, the highest resale transaction in the Outside Central Region occurred at Bedok Residences, where a unit changed hands for S$4.5 million. Located above Bedok Mall and directly integrated with Bedok MRT interchange in District 16, Bedok Residences is a 99-year leasehold mixed-use development completed in 2015 by CapitaLand.

The project comprises 583 residential units sitting atop a retail podium, offering residents immediate access to shops, supermarkets, dining options, and transport connectivity. Its integrated nature continues to support strong buyer interest, particularly among families and investors who value convenience and rental potential.

Wrapping up

January 2026’s condo resale data does not point to a market losing steam. Instead, it reflects one that is stabilising after several years of strong price growth. Prices continue to edge upward on an annual basis, capital gains remain healthy, and high-value transactions still surface across all regions.

At the same time, easing volumes signal that buyers have become more selective and disciplined, especially in the mass-market segment where affordability considerations weigh more heavily.

The post Condo resale prices held firm despite decreased activity levels in January 2026 appeared first on .