After a relatively cautious start to the year, February’s flash data suggests that the condo resale market has begun to regain its footing. Both prices and transaction volumes moved higher, pointing to a return of buyer activity after the seasonal lull in January. More notably, this recovery has pushed overall resale prices to a new all-time high, reinforcing the resilience of the private housing market.

Table of contents

- New resale price peak supported by city fringe demand

- Transaction volumes rebound: +17.5% month-on-month

- Demand profile points to genuine buyers over speculation

- Overall profitability improves, but varies across districts

- Highest condo resale transactions in February 2026

New resale price peak supported by city fringe demand

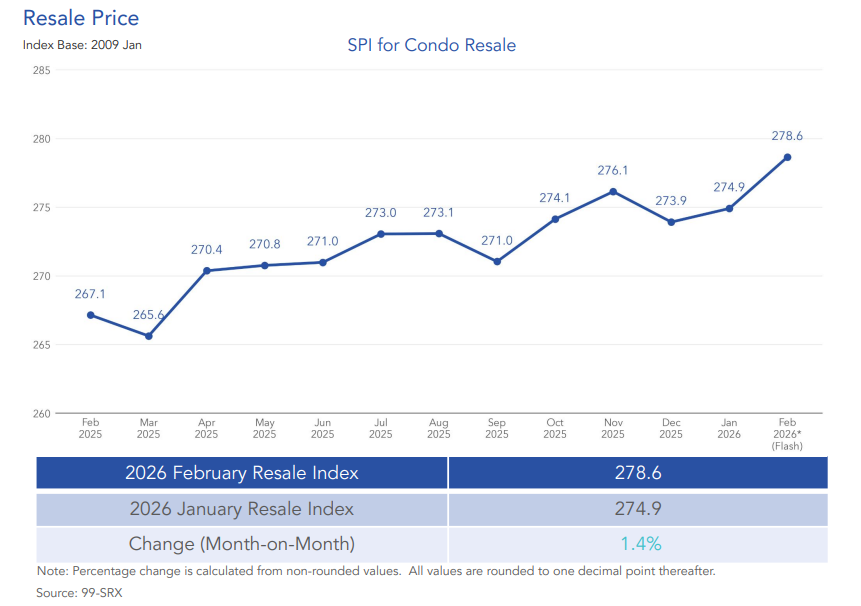

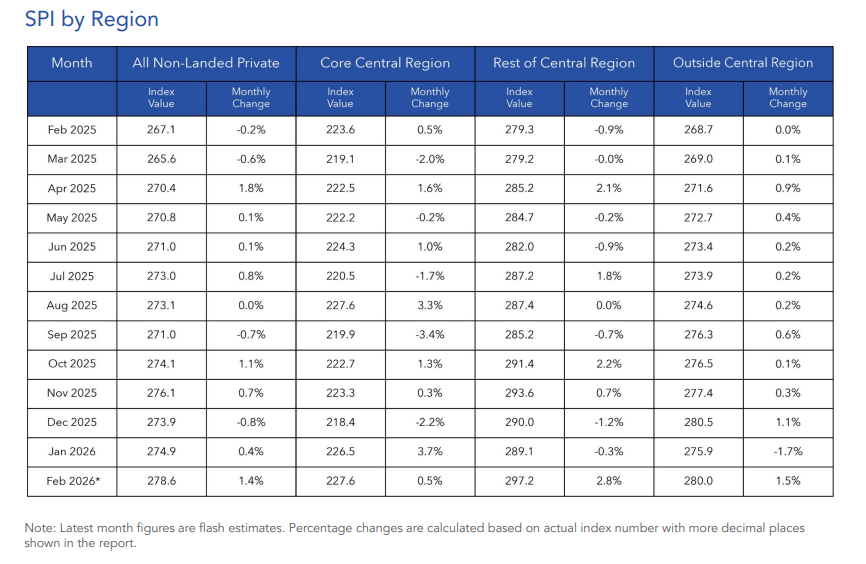

Resale condo prices rose by 1.4% month-on-month in February, bringing the overall price index to 278.6 — a fresh peak for the market. This surpasses January’s 274.9 and marks a continuation of the gradual upward trend seen over the past year.

Mr Luqman Hakim, Chief Data & Analytics Officer at 99.co, highlighted the broader significance of the price movement: “On a year-on-year basis, price growth remains firm at 4.3%, reinforcing the view that underlying support for condo values is still intact.”

The gains seen in February were led by the Rest of Central Region (RCR), which saw prices climb 2.8%. The Outside Central Region (OCR) followed at 1.5%, while the Core Central Region (CCR) posted a more modest 0.5% increase. This distribution highlights a familiar pattern: demand continues to favour city-fringe and mass-market locations where buyers perceive better value.

On a year-on-year basis, this trend becomes even more pronounced. RCR prices have risen by 6.4%, outpacing OCR at 4.2% and CCR at 1.8%. The stronger growth in the city fringe suggests sustained demand for homes that balance central accessibility with relative affordability. In contrast, the more subdued growth in CCR indicates that higher price points continue to temper demand in prime districts, especially in a market where buyers remain selective.

This also suggests that the new price high is not driven by speculative activity in prime districts, but rather by broad-based demand across more accessible segments. In other words, the record index level reflects underlying market depth rather than isolated luxury transactions.

Transaction volumes rebound: +17.5% month-on-month

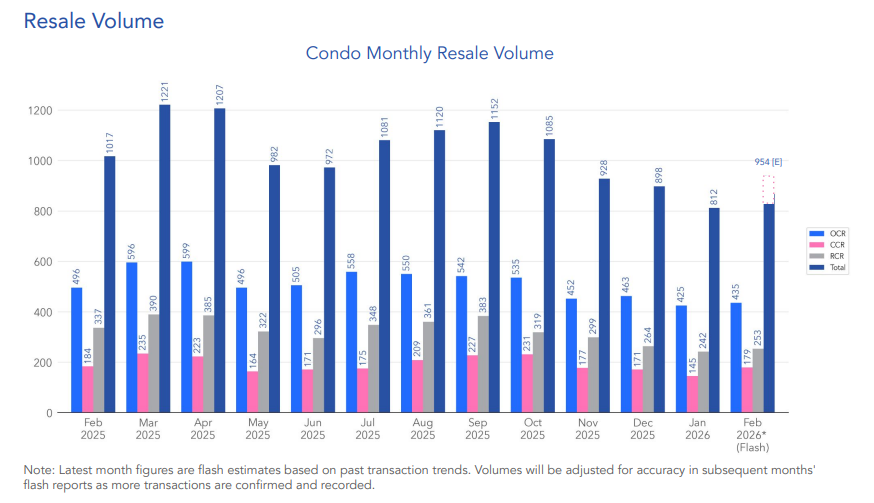

In terms of activity, condo resale volumes rose to an estimated 954 units in February, up 17.5% from January’s 812 units. While this appears to be a strong recovery, it is important to view it in context. January is typically affected by year-end holidays and festive slowdowns, so activity tends to dip before rebounding in the following month. As such, February’s increase likely reflects delayed decisions being carried forward rather than a surge in fresh demand.

Even with the rebound, volumes remain 6.2% lower than February last year. This suggests that while activity has normalised, it has not fully returned to previous highs. Still, transaction levels are 6.7% above the five-year average for February, indicating that the market remains active on a longer-term basis.

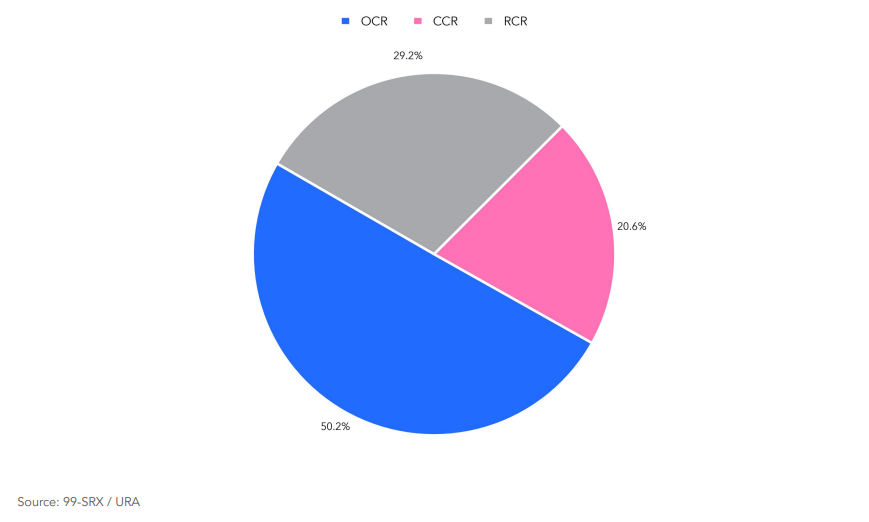

Regionally, OCR transactions made up 50.2% of total volume in February 2026, followed by RCR at 29.2% and CCR at 20.6%. The continued dominance of OCR highlights the strength of upgrader demand, particularly from HDB households entering the private market.

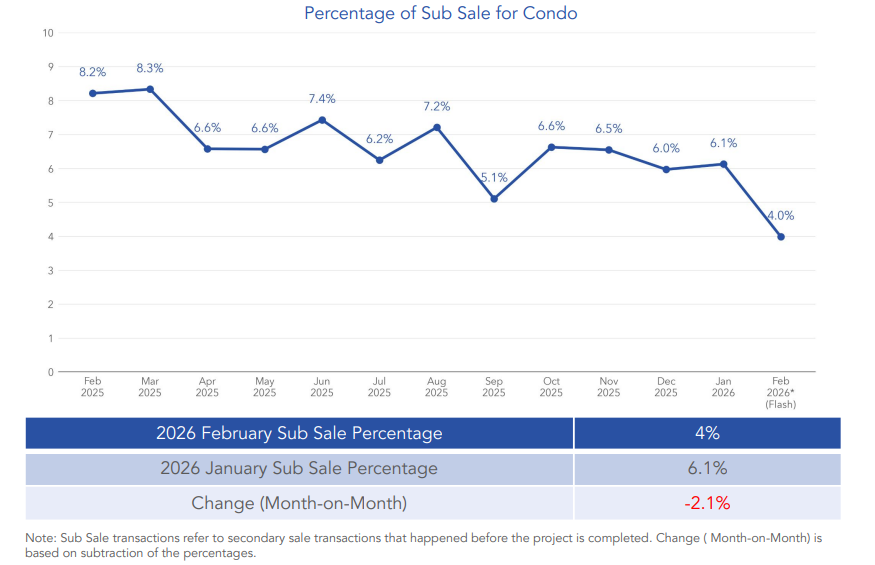

Demand profile points to genuine buyers over speculation

Beyond headline figures, February’s data suggests a market driven more by genuine housing demand than speculative activity. One key indicator is the decline in sub-sale transactions, which fell to 4% of total secondary sales, down from 6.1% in January.

Sub-sales typically involve investors exiting units before project completion. A lower proportion indicates that fewer buyers are engaging in short-term trades, and more are holding properties with a longer-term view.

Combined with the strong showing in OCR and RCR, these points point to a buyer profile dominated by owner-occupiers and upgraders. These buyers tend to be more price-sensitive but also more committed, which contributes to a steadier and less volatile market.

Overall profitability improves, but varies across districts

Sellers continued to hold firm in February. Prices reached a new high while transaction volumes also rose, which suggests that deals are closing with minimal need for discounts. This points to a market where pricing expectations between buyers and sellers are increasingly aligned.

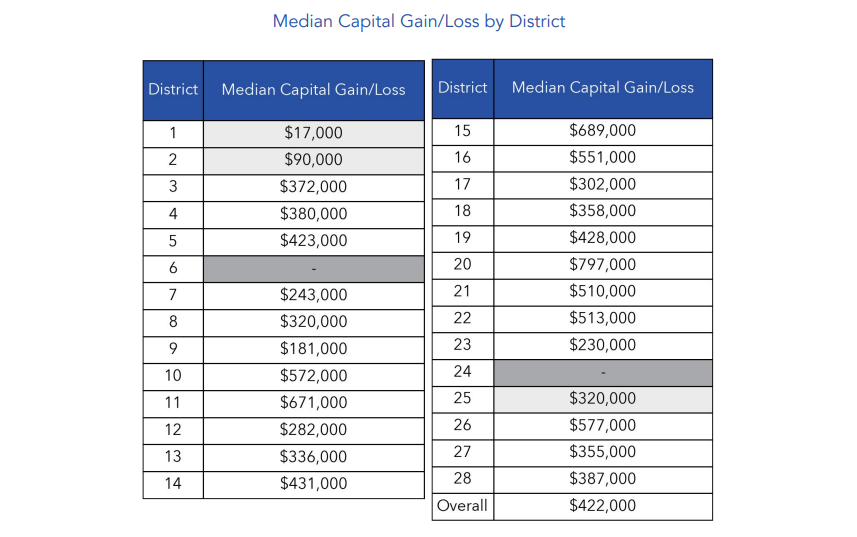

Against this backdrop, overall profitability improved. The median capital gain climbed to S$422,000, up from S$375,000 in January, reflecting stronger resale outcomes as price momentum picked up. In simple terms, more sellers are exiting with meaningful gains, supported by the steady upward trend in resale values.

That said, performance remains highly location-dependent. District 20 (Ang Mo Kio / Bishan / Thomson) recorded the highest median capital gain at S$797,000, while District 9 (Orchard / River Valley) lagged at S$181,000. This gap highlights how entry price and demand depth continue to shape eventual resale outcomes.

For many savvy investors, the strategy has shifted toward acquiring freehold boutique developments like Arina East Residences, which offer a lower entry quantum than traditional CCR luxury homes but benefit from the RCR’s superior price resilience.

Note: Capital gains and returns are calculated by comparing each current transacted price with the previous transacted price of the same unit. Districts with fewer than 10 matching transactions are excluded from the ranking.

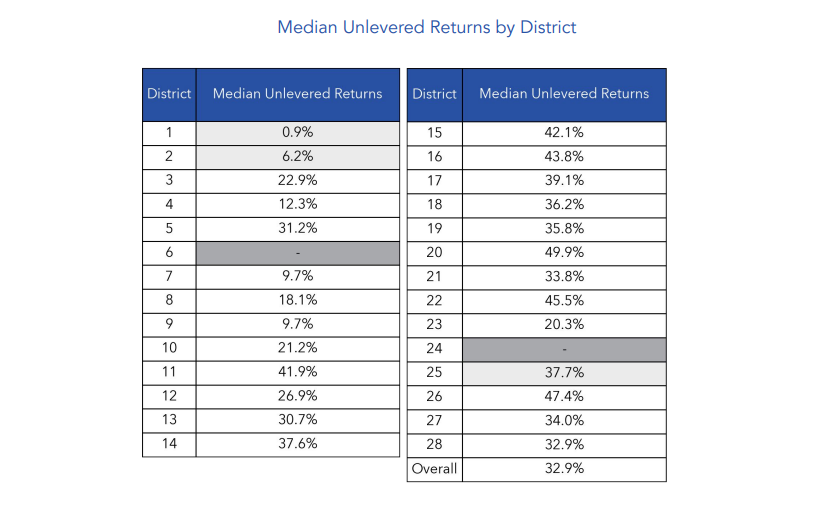

The same pattern appears when looking at returns. Median unlevered returns came in at 32.9%, with District 20 leading at 49.9% and District 9 trailing at 9.7%. While prime districts still command a price premium, the data shows that city-fringe and suburban locations often deliver stronger percentage gains over time, especially when buyers enter at more accessible price points.

Highest condo resale transactions in February 2026

CCR: Leedon Residence – S$16.3 million

The highest resale transaction for the month was recorded at Leedon Residence, where a unit changed hands for S$16.3 million. Located in District 10, this freehold development sits within the prestigious Leedon Heights enclave, an area known for its low-density surroundings and proximity to Holland Village and the Orchard Road belt.

Leedon Residence is a luxury project developed by GuocoLand, featuring large-format units and expansive grounds. Transactions at this level are typically driven by high-net-worth buyers seeking exclusivity, space, and a prime address. While CCR price growth has been more measured, such deals show that demand for trophy assets remains intact.

RCR: Regency Suites – S$6 million

In the RCR, the highest transaction was recorded at Regency Suites, with a resale unit sold for S$6 million. Situated along Kim Tian Road in District 3, the development is within the mature Tiong Bahru estate, a location known for its strong city-fringe appeal.

Regency Suites is a freehold boutique development with a limited number of units, offering a quieter residential environment while remaining close to the CBD. Its proximity to Tiong Bahru MRT station, as well as a well-established mix of cafes, heritage shophouses, and amenities, continues to attract buyers who prioritise both character and convenience.

OCR: Botannia – S$4.58 million

In the OCR, the top resale transaction was recorded at Botannia, where a unit was sold for S$4.58 million. Located along West Coast Road in District 5, Botannia stands out as a rare development with a 956-year leasehold tenure, which often positions it closer to freehold properties in the eyes of buyers.

Completed in 2009, Botannia is known for its luxurious resort-style concept, featuring expansive landscaping and a wide range of facilities. Units here are also generally larger than those in more recent launches, which adds to their appeal among families and buyers who prioritise space and privacy.

The post Condo resale prices hit new high as demand returns in February 2026 appeared first on .