The Urban Redevelopment Authority (URA) and Housing & Development Board (HDB) have released their Q1 2026 flash estimates, offering a snapshot of how Singapore’s housing market started the year. While overall private home prices continued to edge up, HDB resale prices recorded their first quarterly decline in nearly seven years.

Table of contents

- Private home prices inch up by 0.3% q-o-q

- Non-landed price growth led by OCR

- Developer sales boost overall transactions

- HDB resale prices see first quarterly dip in 7 years

- 4.5% y-o-y drop in activity despite quarterly increase

- Million-dollar flats segment remains firm

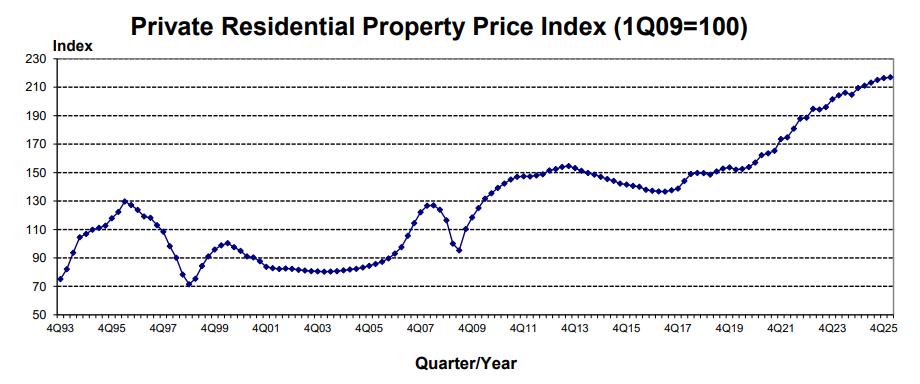

Private home prices inch up by 0.3% q-o-q

According to URA flash estimates, overall private residential prices rose by 0.3% quarter-on-quarter in Q1 2026. This marks a slowdown from the 0.6% growth recorded in the previous quarter and represents the softest increase in six quarters.

The moderation does not point to weakening demand across the board. Instead, it reflects a market that is consolidating after a strong run in the second half of 2025, when new launches drove a surge in activity.

With fewer projects introduced in Q1 2026 and seasonal factors at play, transaction volumes naturally eased, falling by about 40% on a quarter-on-quarter basis. At the same time, price growth remained intact, supported by continued demand across both new launches and the broader private housing market.

Looking deeper, the performance across segments reveals a more nuanced picture. Non-landed private homes led growth, rising 1.0% quarter-on-quarter and reversing the slight decline seen in Q4 2025. In contrast, landed home prices fell by 1.8%, weighed down by weaker transaction volumes.

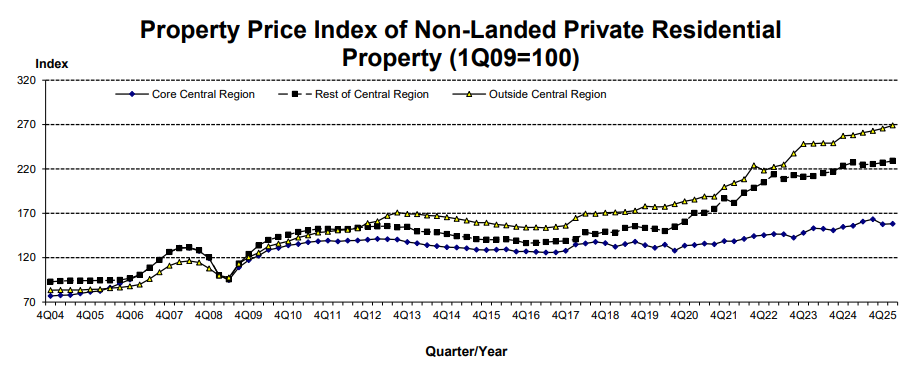

Non-landed price growth led by OCR

Across regions, the Outside Central Region (OCR) recorded the strongest growth at 1.3% quarter-on-quarter, extending its momentum from the previous quarter. The Rest of Central Region (RCR) followed with a 0.9% increase, while the Core Central Region (CCR) posted a modest 0.4% gain, rebounding from its earlier decline.

The relatively narrower pricing gap between CCR and RCR developments also appears to have sharpened buying interest in prime areas, as the perceived value proposition improved for buyers who were previously priced out of the CCR.

Developer sales boost overall transactions

Sale transaction volume (up to mid-March) totalled 4,041 in Q1 2026, compared to 6,699 in Q4 2025. Mr Luqman Hakim, Chief Data & Analytics Officer at 99.co, notes that buyer demand has increasingly centred on the primary market, particularly in the OCR, where new launches continue to draw strong interest.

This is evident in the performance of Pinery Residences, a 588-unit development in Tampines West, which recently moved 544 units at an average price of S$2,546 psf during its launch weekend, translating to a take-up rate of 92.5%.

“Buyers are gravitating towards new launches, where pricing, incentives, and product offerings are perceived to be more attractive compared to resale options,” Mr Luqman explains.

| Project | Region | Total Units | Total Sold | Average PSF |

| Newport Residences | CCR | 246 | 183 | S$3,162 |

| River Modern | CCR | 455 | 413 | S$3,267 |

| Nara Residences | OCR | 540 | 138 | S$2,154 |

| Pinery Residences | OCR | 588 | 544 | S$2,546 |

Based on URA developers’ sales data and caveats lodged up till 22 March, developers sold an estimated 1,355 new private homes (ex. EC) and 1,087 new EC units. New private home sales could approach 2,000 units for the quarter when the full set of transactions is accounted for. In contrast, the resale segment saw 2,662 units transacted as of mid March, likely falling short of the 3,529 resale transactions recorded in the previous quarter.

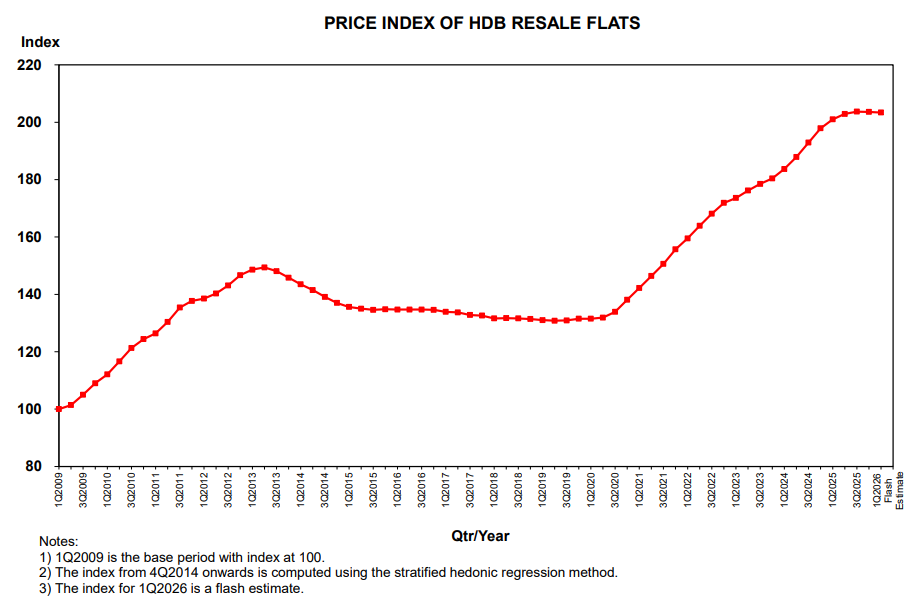

HDB resale prices see first quarterly dip in 7 years

In contrast, flash estimates from the HDB show that the resale price index declined by 0.1% quarter-on-quarter in Q1 2026. This marks the first quarterly drop since Q2 2019, ending a prolonged period of modest but steady price growth. While the decline is marginal, it signals an important turning point for the public housing market: After several years of gains, conditions are starting to rebalance.

One of the key drivers behind this shift is the increase in supply. A significant number of flats are reaching their five-year Minimum Occupation Period (MOP), allowing them to enter the resale market. At the same time, new Build-to-Order (BTO) and Sale of Balance Flats (SBF) exercises have expanded options for buyers.

Mr Luqman highlights how these factors are shaping the market outlook. “HDB’s flash estimate showing a 0.1% decline in resale prices in 1Q 2026 aligns with the 13,484 flats reaching MOP this year,” he says. “With more newly eligible flats entering the resale market, price growth is likely to remain subdued over the course of the year.”

4.5% y-o-y drop in activity despite quarterly increase

With more supply entering the market, flash estimates from the HDB also show that resale transaction volumes rose 17.6% quarter-on-quarter to 6,179 units in Q1 2026. This increase suggests that activity has picked up in the short term.

However, the stronger quarterly showing does not necessarily point to renewed upward pressure on prices. Instead, it indicates that buyers are becoming more selective, with greater room to negotiate as options expand.

On a year-on-year basis, resale volumes were still 4.5% lower than in Q1 2025. The growing supply pipeline has eased the urgency to purchase, particularly for buyers who now have viable alternatives such as shorter-waiting-time flats and Sale of Balance Flats (SBF) exercises. As a result, while transactions remain relatively healthy, the balance of power is gradually shifting, with buyers taking a more measured approach in the resale market.

Million-dollar flats segment remains firm

At the same time, million-dollar flat transactions continued to rise, reaching 412 units in Q1 2026. This marks a 17.4% increase from the previous quarter, when 351 such transactions were recorded. Despite the increase, these high-value deals still make up a relatively small portion of the overall resale market. They accounted for just 6.9% of total transactions during the quarter, suggesting that while headline prices remain eye-catching, they are not representative of broader market conditions.

Additionally, these high-value transactions continue to be concentrated in mature estates and city-fringe locations, where strong amenities and central connectivity support pricing. The latest headline deal came from Tiong Bahru View in Bukit Merah, where a 5-room flat changed hands for S$1.648 million. This transaction now ranks among the top three highest HDB resale prices recorded, with the top two spots still held by earlier deals at SkyTerrace @ Dawson in Queenstown.

It is also worth noting that the average transacted price for these million-dollar flats came in at around S$1.15 million, which is lower than the previous quarter. This indicates that while more million-dollar deals are taking place, price points within this segment may be stabilising, as the wider resale market begins to moderate.

Wrapping up

In the private housing segment, prices continue to hold up, supported by strong take-up at new launches, particularly in the OCR, where relative affordability and well-positioned projects continue to attract buyers. The HDB resale market, however, is entering a different phase. An expanding supply of flats, alongside a broader range of housing options, has started to ease price pressures and shift the market towards a more balanced state.

This divergence highlights how different buyer groups are responding to current conditions. Private home buyers, including upgraders and investors, are still actively deploying capital into new launches that offer compelling value and long-term potential. In contrast, HDB buyers now have greater flexibility and choice, which reduces urgency and naturally tempers price growth across the resale market.

Note: The flash estimates are compiled based on transaction prices submitted up to mid-March. The statistics will be updated on 24 April 2026 when URA releases its full set of real estate statistics for the 1st Quarter 2026.

The post URA and HDB flash estimates show diverging price trends for private and public housing in Q1 2026 appeared first on .