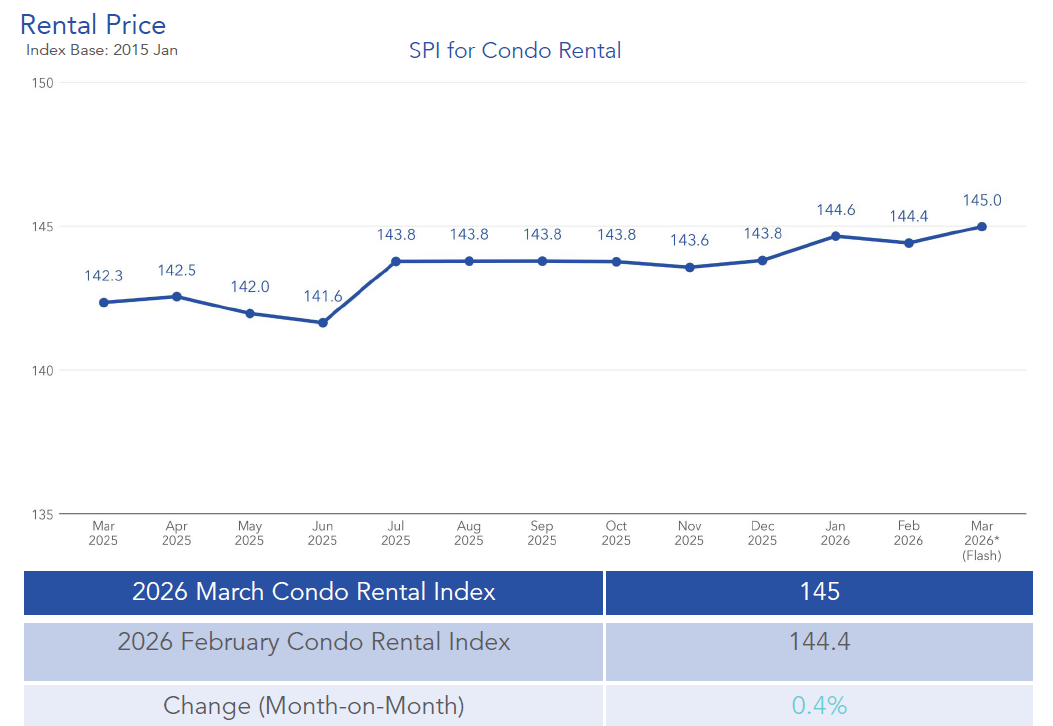

Singapore’s rental market showed clear signs of stabilising in March 2026, even as activity picked up. Condo and HDB rents continued to inch upwards, but the pace of growth remained measured. Notably, this steady increase has pushed the condo rental market to a new milestone, with the Condo Rental Price Index (SPI) reaching a record high of 145 in March 2026. This suggests that while growth is gradual, price levels remain elevated. At the same time, rental volumes rebounded across both segments, largely due to seasonal factors rather than a sudden surge in demand.

So, what does this mean for you? On one hand, landlords are still seeing some room for rental growth. On the other, tenants are becoming more price-conscious, which is naturally keeping increases in check. As a result, the market is settling into a more balanced phase, where affordability and practical needs play a bigger role in shaping demand.

Table of contents

- Condo rents edge up to new all-time high, but the pace remains measured

- Condo rental volumes rebound after February lull

- HDB rents see slower growth amid price sensitivity

- HDB rental volumes rise, but remain softer year-on-year

- Demand patterns reflect affordability and practical needs

- A market that is stabilising, not surging

Condo rents edge up to new all-time high, but the pace remains measured

In March 2026, condo rental prices continued their gradual climb, rising by 0.4% compared to the previous month. While this marks another month of growth, the increase remains modest, suggesting that the rental market is beginning to stabilise rather than accelerate.

At the same time, this latest increase has pushed the Condo Rental Price Index (SPI) to a record high of 145, reflecting how rents have built up over time. In other words, while prices are now at an all-time high, the pace of growth has slowed, pointing to a market that is levelling off rather than overheating.

When you look closer, a mixed picture across regions can be seen. Prices in the Core Central Region (CCR) and Rest of Central Region (RCR) grew by 0.4% and 1.1%, respectively. Meanwhile, rents in the Outside Central Region (OCR) dipped slightly by 0.3%. This suggests that while demand in central locations remains firm, price resistance is starting to show in more suburban areas.

On a year-on-year basis, overall condo rents were 1.9% higher than in March 2025. Across regions, CCR rents rose by 2%, RCR by 1.9%, and OCR by 0.9%. Although these gains are not insignificant, they are still relatively controlled when compared to the sharper spikes seen in earlier periods.

As Mr. Luqman Hakim, Chief Data & Analytics Officer at 99.co, points out, “What we are seeing is a market that is no longer surging, but instead adjusting. Tenants are becoming more mindful of costs, and that naturally limits how far rents can climb.”

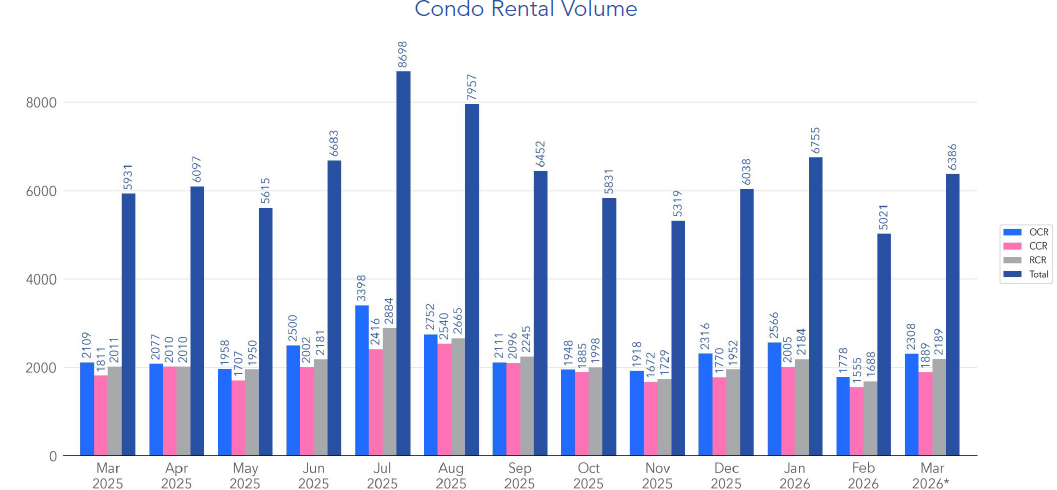

Condo rental volumes rebound after February lull

Even as price growth remained modest, rental activity picked up significantly. Condo rental volumes surged by 27.2% month-on-month, with an estimated 6,386 units rented in March, up from 5,021 in February.

At first glance, this increase may suggest a sudden spike in demand. However, the underlying reason is more nuanced. February tends to be a shorter month, and it is often affected by festive periods that slow down transaction activity. As such, many deals are likely pushed into March, creating a catch-up effect.

Mr. Hakim explains this trend clearly, “The rebound in March is largely seasonal. While demand is still present, part of the increase comes from transactions that were delayed earlier.”

Even so, the broader trend remains healthy. On a year-on-year basis, rental volumes were 7.7% higher than in March 2025. In addition, volumes came in 8% above the five-year average for the month, which suggests that overall leasing activity is still relatively robust.

Looking at the distribution across regions, the OCR accounted for the largest share of rental activity at 36.1%. This was followed by the RCR at 34.3%, and the CCR at 29.6%. This breakdown shows that while central locations remain attractive, a significant portion of tenants continue to prioritise more affordable options outside the core districts.

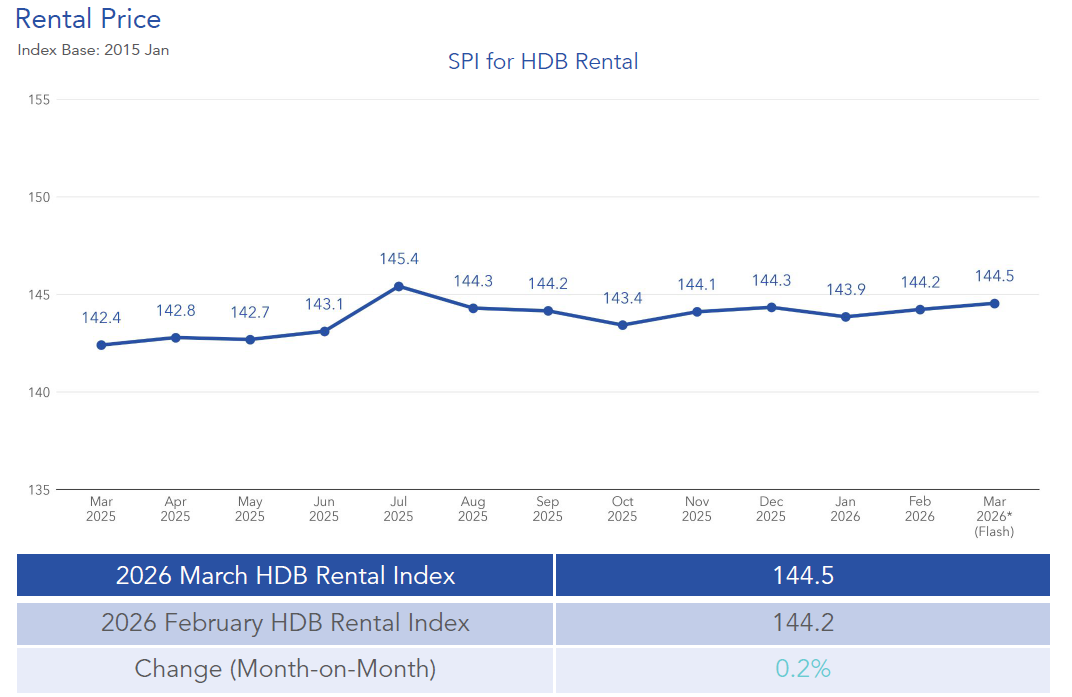

HDB rents see slower growth amid price sensitivity

Turning to the HDB segment, rental prices also increased in March, but at a slower pace. Overall rents edged up by 0.2% compared to February, reflecting a more cautious market environment.

According to Mr. Hakim, “Affordability remains a key factor in the HDB rental segment. Tenants in this market are generally more budget-conscious, so rent increases tend to be smaller and more gradual.”

Within the HDB market, price movements varied across flat types and locations. Rents in Mature estates remained unchanged, while those in Non-Mature estates rose by 0.5%. By flat type, 3-room and 5-room units saw increases of 0.7% and 0.8%, respectively. In contrast, 4-room flat rents held steady, and Executive flats experienced a decline of 1.4%.

On a year-on-year basis, overall HDB rents were 1.5% higher than in March 2025. Both Mature and Non-Mature estates recorded similar increases of around 1.5% and 1.4%. Across flat types, 3-room, 4-room, and 5-room units posted gains between 1.2% and 1.8%, while Executive flats saw a slight drop of 0.8%.

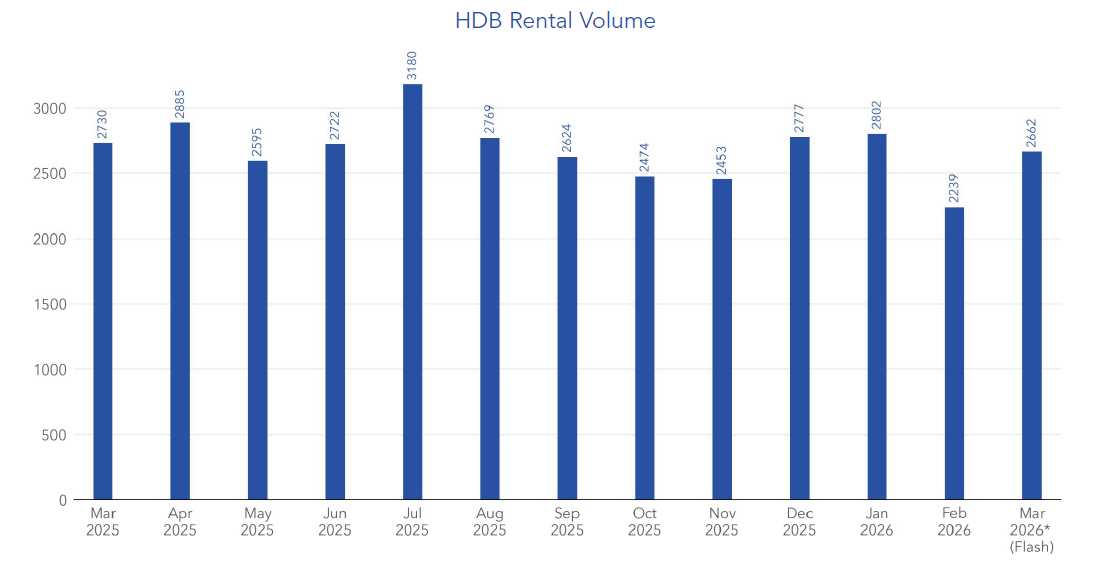

HDB rental volumes rise, but remain softer year-on-year

Similar to the condo market, HDB rental volumes also saw a noticeable increase in March. Transactions rose by 18.9% month-on-month, with an estimated 2,662 flats rented, up from 2,239 in February.

Again, this rebound can largely be attributed to seasonal factors. The slowdown in February likely pushed some rental activity into March, resulting in a temporary spike.

However, when you take a step back, a different trend emerges. Despite the monthly increase, rental volumes were 2.5% lower than in March 2025. Furthermore, they remained 5.9% below the five-year average for the month.

This suggests that while demand is still present, it has eased compared to previous years. One possible reason is that more renters are transitioning into homeownership, especially as the resale market becomes more stable and accessible.

Demand patterns reflect affordability and practical needs

Breaking down the rental activity further, 4-room flats made up the largest share of HDB rentals in March at 36.6%. This was followed by 3-room flats at 33.4%, 5-room flats at 24.4%, and Executive flats at 5.6%.

This distribution points to a clear trend. Most tenants continue to prioritise practical and affordable housing options, with mid-sized flats remaining the most popular choice.

At the same time, demand in both the condo and HDB segments continues to be supported by transitional housing needs. These include individuals waiting for new homes to be completed, as well as those seeking temporary accommodation due to life changes.

A market that is stabilising, not surging

Taken together, the March 2026 data paints a picture of a rental market that is stabilising. Prices are still rising, but at a controlled pace. Meanwhile, rental volumes have rebounded, although much of this can be attributed to seasonal factors rather than a sharp increase in demand.

For you as a renter or landlord, this means that conditions are becoming more predictable. While opportunities still exist, decisions are now more likely to be shaped by affordability and long-term considerations, rather than short-term momentum.

The post Condo rental prices hit record high as HDB rents edge up and activity rebounds appeared first on .