April 2026 brings a clearer view of how the HDB resale market is evolving. While headline figures show slight changes in both prices and activity, the underlying trends point to a shift in buyer behaviour and market dynamics.

Table of contents

- HDB resale prices ease slightly in April 2026

- Price trends across flat types show mixed movement

- Resale volumes decline more noticeably

- Record-breaking transaction shows demand for prime units

- Million-dollar flats see slight dip in numbers

- Market enters a phase of recalibration

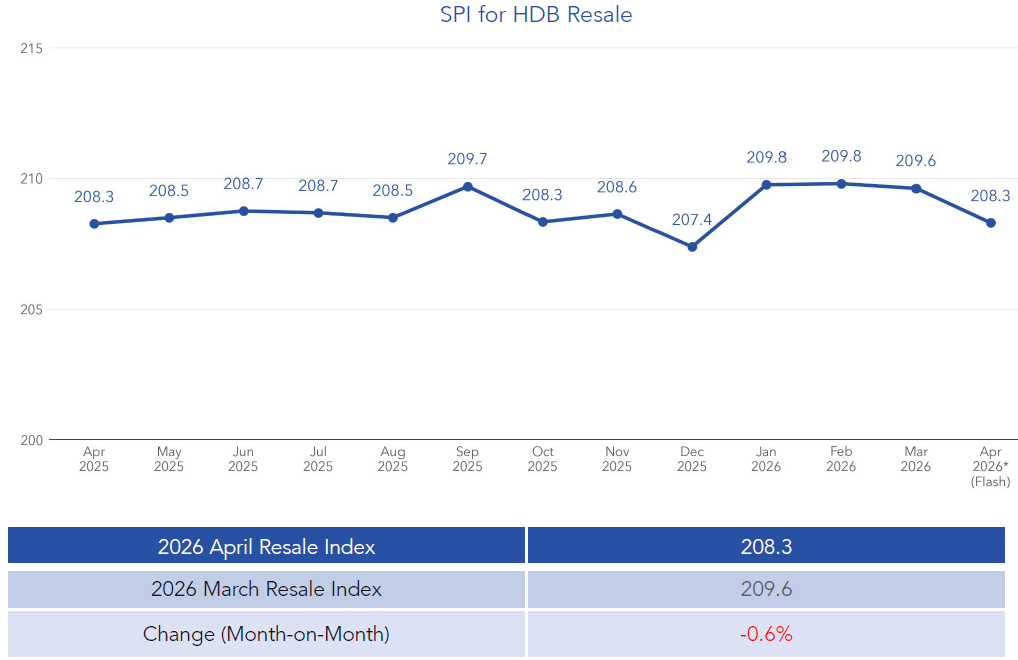

HDB resale prices ease slightly in April 2026

In April 2026, the HDB resale market showed signs of easing after several months of firmer performance. Overall, resale prices dipped by 0.6% month-on-month, pointing to a shift in momentum.

Mr. Luqman Hakim, Chief Data & Analytics Officer at 99.co, shared that April’s figures reflect a market that is gradually returning to more typical conditions. According to him, prices are softening slightly, while transaction volumes are falling more noticeably. As a result, both buyers and sellers are now adjusting their expectations, even though the market remains generally stable.

When you look deeper into the numbers, prices in Mature Estates declined by 1.4%, while those in Non-Mature Estates saw a smaller drop of 0.4%. This suggests that even traditionally stronger locations are experiencing some resistance from buyers.

Price trends across flat types show mixed movement

Across different flat types, price movements were uneven. Prices for 3-room flats fell by 0.9%, while 5-room flats saw a sharper decline of 1.7%. Executive flats also recorded a drop of 1.3%. Meanwhile, 4-room flats stood out as the only category to post a slight increase, rising by 0.1%.

This variation highlights how demand is shifting across different buyer segments. While larger flats may be facing more resistance due to higher price points, 4-room flats continue to appeal to a broader group of buyers.

Looking at the year-on-year data, however, a clearer picture of stability emerges. Overall prices remained largely unchanged compared to April 2025. In fact, 4-room and 5-room flats still recorded small gains of 0.4% and 0.2%, respectively. On the other hand, 3-room and Executive flats saw slight declines of 0.8% each.

In terms of location, prices in Mature Estates edged up by 0.1% over the past year, while Non-Mature Estates saw a marginal decline of 0.2%. Mr. Luqman noted that the 0.6% dip suggests that buyer resistance is beginning to emerge, especially after a period where prices held relatively firm. However, since prices remain broadly flat year-on-year, this change is likely temporary rather than structural.

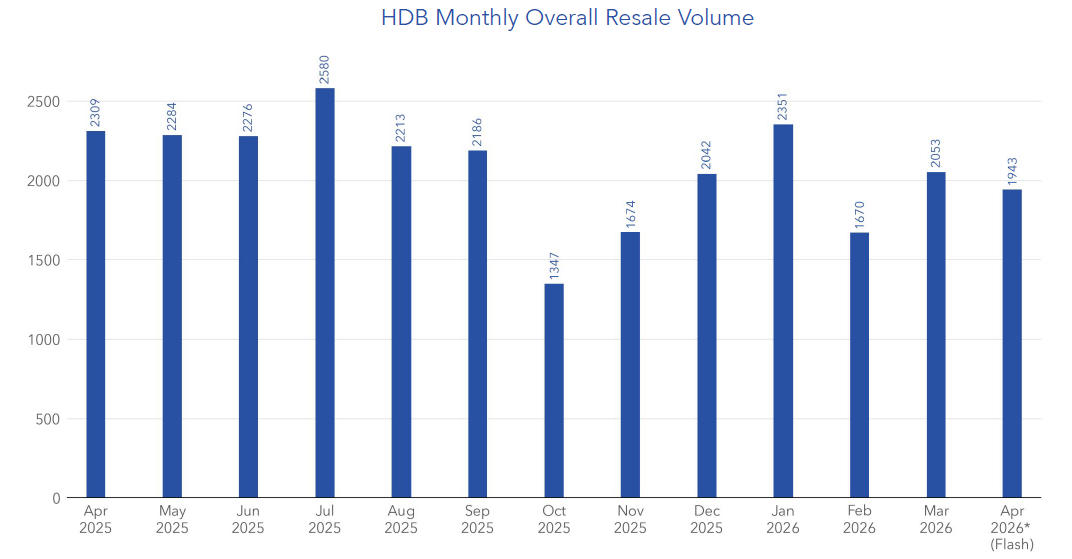

Resale volumes decline more noticeably

While prices only slipped slightly, transaction volumes saw a more noticeable pullback. A total of 1,943 resale flats were transacted in April 2026, marking a 5.4% decrease from March.

On a year-on-year basis, the decline was even more pronounced, with volumes falling by 15.9%. This indicates that fewer deals are being completed, even as prices remain relatively stable.

Breaking the numbers down further, 4-room flats continued to make up the largest share of transactions at 44.7%. This was followed by 3-room flats at 25.6%, 5-room flats at 23.3%, and Executive flats at 6.4%. Non-Mature Estates accounted for the majority of transactions, making up 56.7% of total resale volume. Meanwhile, Mature Estates contributed 43.3%.

Mr. Luqman explained that the decline in both price and volume can be linked to a more cautious global economic outlook. This has affected buyer sentiment, making some households more careful about entering the market. At the same time, supply is gradually increasing, as more flats reach their Minimum Occupation Period (MOP). In 2026 alone, around 13,000 flats are expected to reach MOP. As these units enter the resale market, buyers are presented with more options, which in turn reduces urgency and puts some pressure on prices.

Record-breaking transaction shows demand for prime units

Despite the softer market conditions, high-value transactions are still taking place. In April 2026, the highest resale price recorded was S$1,728,000 for a 5-room flat at City Vue @ Henderson.

Read more: 5-room HDB in Bukit Merah sets new official national record at S$1.728M

This transaction highlights that while the broader market may be slowing, premium flats with strong attributes continue to command top prices. Factors such as location, views, high floor levels, and proximity to amenities often play a key role in driving such outcomes. Mr. Luqman pointed out that this record deal shows price ceilings are still being tested. In other words, demand for rare and well-located flats remains resilient, even as overall activity moderates.

In Non-Mature Estates, the highest transacted price was S$1,180,000 for an Executive flat located along Woodlands Street 81. This further shows that strong pricing is not limited to central areas alone.

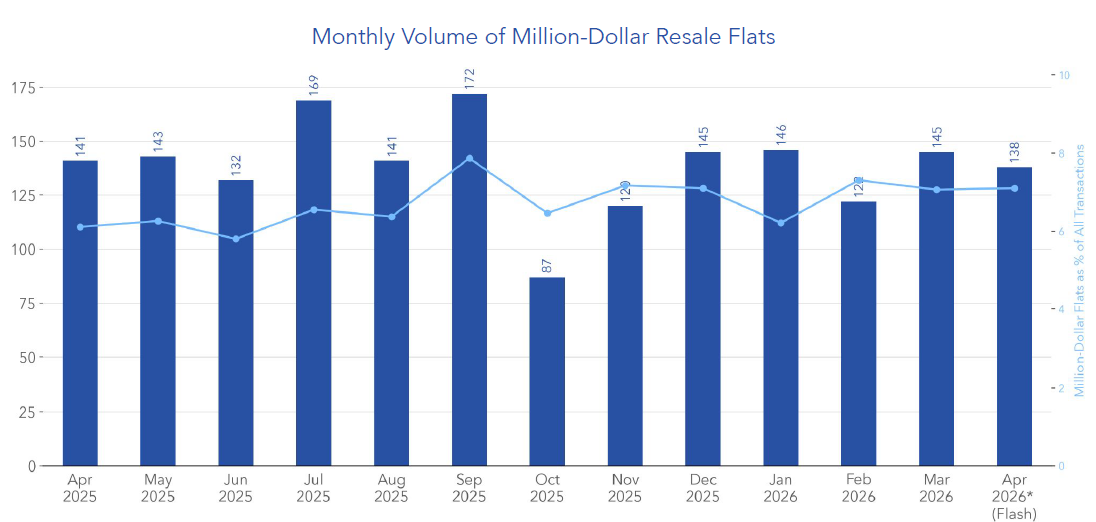

Million-dollar flats see slight dip in numbers

Another key trend in April was the slight decline in million-dollar transactions. A total of 138 flats were sold1 for at least S$1 million, down from 145 units in March.

These transactions made up 7.1% of total resale volume for the month. While this is slightly lower than the previous month, the figure still reflects a significant presence of high-value deals in the market.

Looking at the distribution, Queenstown recorded the highest number of million-dollar flats with 21 transactions. This was followed by Toa Payoh with 17 units, and Ang Mo Kio with 15 units.

Beyond these towns, million-dollar deals were also seen across a wide range of estates. These included Bukit Merah, Kallang/Whampoa, Tampines, Woodlands, Bishan, the Central Area, Bedok, Clementi, Geylang, Hougang, Serangoon, Jurong East, Pasir Ris, Bukit Timah, Punggol, Sengkang, Bukit Panjang, and Yishun.

This wide spread shows that million-dollar flats are no longer limited to a few select locations. Instead, they are becoming more common across different parts of Singapore, especially for larger or well-located units.

Market enters a phase of recalibration

Overall, April 2026 reflects a market that is adjusting rather than declining. Prices have softened slightly, while volumes have pulled back more clearly. At the same time, underlying stability remains intact.

Even so, the presence of record-breaking transactions and a steady number of million-dollar deals suggests that demand has not disappeared. Instead, it has become more measured.

As more MOP flats enter the market and global conditions continue to evolve, the HDB resale market is likely to remain stable, but with a more cautious pace of activity in the months ahead.

- Sold units are based on the resale registration date. Registered resale applications are generally representative of completed resale transactions. ↩︎

The post HDB resale prices and transactions ease slightly in April 2026 appeared first on .