The resale condo market began to show clearer signs of stabilisation in March 2026. While transaction activity continued to pick up, price movements became more restrained. As a result, the market appears to be settling into a more balanced state after the earlier fluctuations at the start of the year.

This sets the tone for the month, where both price and volume trends are no longer moving sharply, but instead adjusting more gradually.

Table of contents

- Prices dip slightly, but growth trend remains intact

- Transaction volumes continue to rise, but at a more measured pace

- Strong new launches continue to compete for demand

- Notable high-value transactions in March

- Capital gains and returns ease slightly

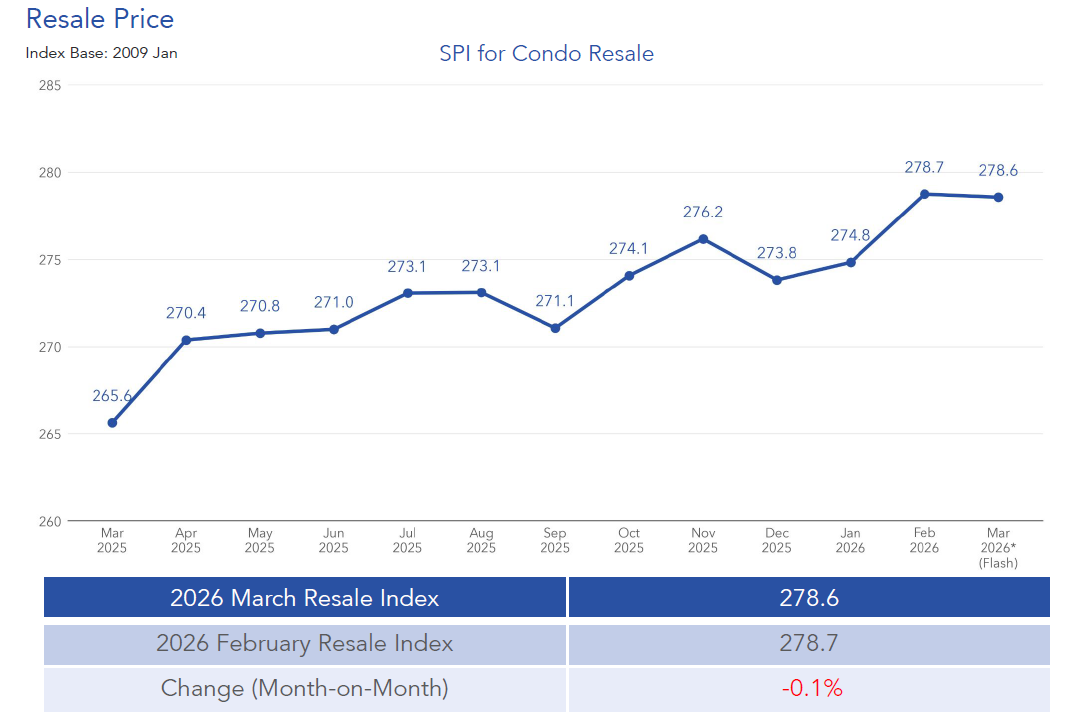

Prices dip slightly, but growth trend remains intact

Price movements in March were relatively mild, with the first slight pullback recorded this year. However, this does not point to a weakening market. Instead, it reflects a slowdown in momentum after a period of steady growth.

As highlighted by Mr. Luqman Hakim, Chief Data & Analytics Officer at 99.co, “On a month-on-month basis, overall resale prices dipped slightly by 0.1%. Even so, prices remain 4.9% higher year-on-year, indicating that the broader upward trend is still intact, albeit at a slower pace.”

Across regions, performance was mixed. The Core Central Region (CCR) and Outside Central Region (OCR) both recorded modest increases of 0.4% and 0.5%, respectively. Meanwhile, the Rest of Central Region (RCR) saw a decline of 1.2%. On a year-on-year basis, all three regions still posted gains. The CCR increased by 4.4%, the RCR by 4.9%, and the OCR by 4.6%.

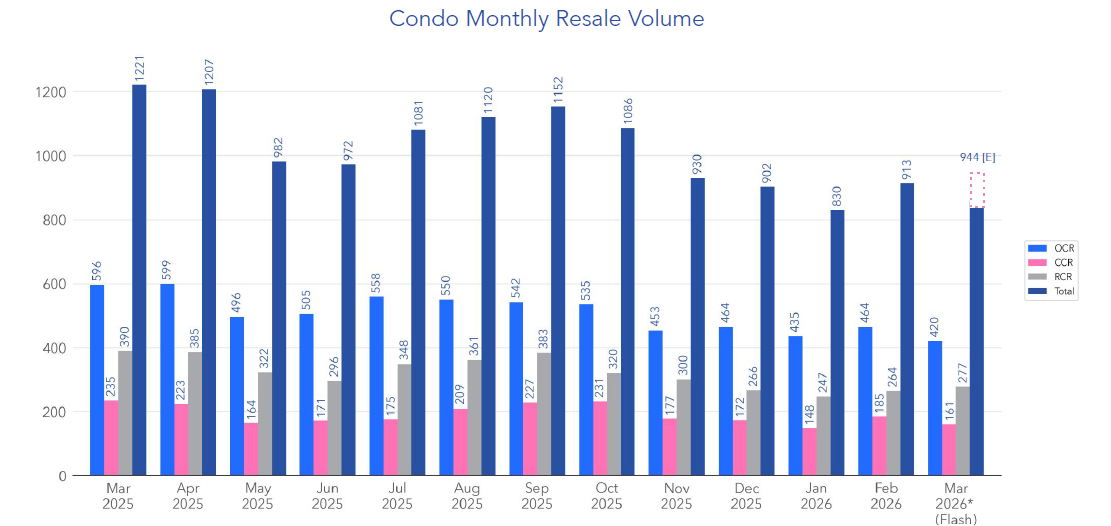

Transaction volumes continue to rise, but at a more measured pace

Resale activity continued to increase in March, although the pace of growth has started to normalise. This comes after a stronger rebound in the previous month.

Mr. Luqman explains, “On the activity front, an estimated 944 units were resold in March, up 3.4% from February. This follows a stronger rebound of about 17% in February after the seasonal slowdown at the start of the year. The more modest increase in March suggests that transaction volumes are stabilising back to more typical levels.”

Even so, resale activity remains lower compared to historical benchmarks. Volumes were 22.7% lower than in March 2025, and about 20% below the five-year average for the same month.

In terms of regional distribution, the OCR accounted for the largest share of transactions at 49%. This was followed by the RCR at 32.3%, and the CCR at 18.8%. This distribution highlights the continued demand for more affordable, mass-market homes.

At the same time, sub-sale transactions made up 4.6% of total secondary sales in March, marking a slight increase from February. These transactions, which occur before a project is completed, often reflect investor activity and shifting expectations around new launches.

Strong new launches continue to compete for demand

At the same time, the primary market played a key role in shaping resale activity. Several new launches saw very strong demand, which likely pulled some buyers away from the resale segment.

As noted by Mr. Luqman, “Recent new launches such as River Modern, Pinery Residences and Rivelle Tampines saw exceptionally strong take-up rates of up to 92.5% at launch. These robust sales likely diverted some demand away from the resale segment, as buyers were drawn to newer projects offering modern layouts and progressive payment schemes.”

Because of this, even though resale volumes increased, the growth may have been more moderate than expected. Buyers today are weighing more options, especially when new developments offer newer designs and staged payment structures.

Still, resale condos remain relevant as they continue to appeal to buyers who prefer immediate move-in, larger layouts, or homes in more established areas.

Read more: Robust new launch take-up pushes March developer sales close to 2,000 units

Notable high-value transactions in March

At the top end of the market, a resale unit at Le Nouvel Ardmore was transacted for S$19.5 million, making it the highest deal recorded for the month. This shows that demand for high-end properties is still present, particularly in prime districts.

Le Nouvel Ardmore is a freehold development located within the Ardmore Park enclave in District 10, an area widely known for its exclusivity and proximity to Orchard Road. Completed in 2014, the project was developed by Wing Tai and designed by internationally recognised architect Jean Nouvel. The development stands out for its limited supply, with just over 40 units housed within a single high-rise tower.

In terms of location, the property sits within walking distance of Orchard MRT, while also being close to established schools and well-known retail destinations. Despite this, the development maintains a sense of privacy, even though it is positioned near one of Singapore’s busiest lifestyle districts. Many units also enjoy expansive views of the city skyline and surrounding areas.

In the RCR, the highest transaction came from The Waterside, where a unit was sold for S$5.78 million. This freehold development along Tanjong Rhu Road is known for its large site and spacious homes.

The project features multiple residential towers with sizeable 3- and 4-bedroom units, many exceeding 2,000 square feet. Depending on the unit’s orientation, views of the sea, Kallang Basin, or the city skyline can be enjoyed. In addition, a full range of facilities such as sports courts, a swimming pool, and a gym is provided.

Its location also supports its appeal. With MRT stations like Mountbatten and Stadium nearby, along with good connectivity to the CBD and Changi Airport, the development remains well-positioned. Schools, leisure options, and dining spots in the surrounding area further add to its suitability for families.

Meanwhile, in the OCR, the highest resale transaction was recorded at The Gazania, where a unit was sold for S$4.2 million. Located within a landed enclave in District 19, this freehold development offers a more private and low-density living environment.

The project consists of several low-rise blocks and offers a range of unit types, from 1- to 4-bedroom apartments, as well as larger formats such as maisonettes and penthouses. Units are designed with natural light in mind, while some feature higher ceilings and more open layouts. Facilities include a lap pool, gym, clubhouse, and landscaped spaces. Its proximity to Bartley MRT, along with nearby schools and amenities, enhances its accessibility and convenience.

Capital gains and returns ease slightly

In terms of investment performance, the overall median capital gain for resale condos in March stood at S$400,000. This represents a decrease of S$24,000 from February.

Across districts, District 10 (Tanglin / Holland / Bukit Timah) recorded the highest median capital gain at S$867,000. On the other hand, District 4 (Sentosa / Harbourfront) posted the lowest median gain at S$164,000.

Similarly, the overall median unlevered return came in at 30.3% in March. District 15 (East Coast / Marine Parade) and District 23 (Dairy Farm / Bukit Panjang / Choa Chu Kang) led the rankings, both recording returns of 42.9%. In contrast, District 2 (Chinatown / Tanjong Pagar) registered the lowest return at 10.1%.

These figures are derived by comparing each unit’s latest transaction price with its previous sale price, offering a clearer view of how individual properties have performed over time.

The post Condo resale prices dip slightly as volumes continue to rise in March 2026 appeared first on .